Two Tools, Different Specialties

We know that funding a buildout requires serious capital. Choosing the right sba 7a vs 504 restaurant loan dictates your long-term success. Our team helps North Carolina operators get the exact equipment and working capital they need.

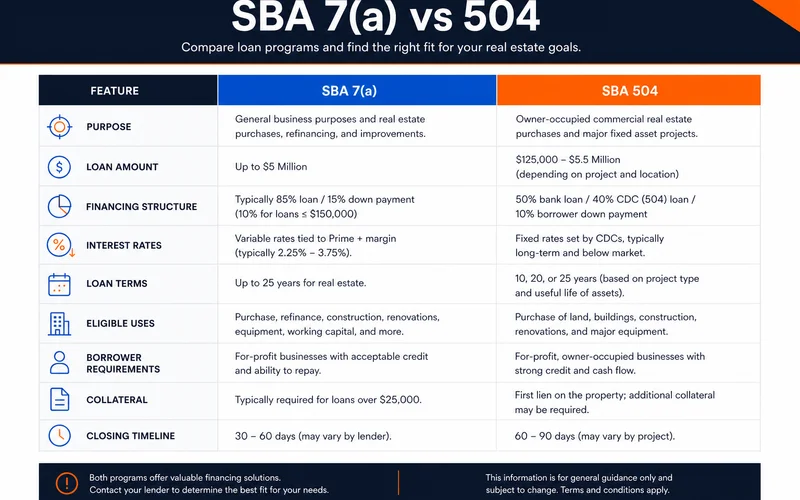

The Small Business Administration provides two distinct programs to solve this financing gap.

- The SBA 504 loan for large fixed assets.

- The SBA 7(a) loan for general working capital.

We evaluate these options every day to fund commercial real estate and business acquisitions. A recent 2026 policy update allows eligible borrowers to combine these programs for up to $10 million in total SBA-backed capital.

We find that choosing the right foundational structure is the most critical first step. The best sba loan restaurant property option depends heavily on your specific asset mix.

Our guide will help you compare the two options directly. You can also review our broader SBA 7(a) financing hub for extra context.

We will break down the specific requirements and walk through the exact deal structures.

Let’s look at the data and find the most profitable path forward.

SBA 504: Built for Real Estate

We always recommend the SBA 504 program for owner-occupied real estate and large fixed assets. This loan structure involves three distinct components.

- 50% from a conventional bank lender at competitive market rates.

- 40% from a Certified Development Company (CDC) at an SBA-fixed rate.

- 10% down payment from the borrower.

Our team likes the 504 because the CDC interest rate is fixed and tied to the 10-year Treasury bond. The CDC portion caps at $5.5 million per project for the 2026 fiscal year. We see this fixed portion hovering around 6.5% to 7.5% as of mid-2026.

Strict occupancy rules apply to this program. Our new construction projects demand a 60% owner-occupancy rate. The SBA mandates that your operating business occupy at least 51% of an existing building.

- Lower effective rate than 7(a) for pure real-estate deals.

- Long terms span up to 25 years for property purchases.

- Fixed-rate options on the CDC portion offer long-term rate certainty.

- Strict use restrictions prevent funding for short-term working capital or inventory.

We regularly see the 504 structure save operators thousands of dollars in interest over a 25-year term. Buying the building under your restaurant often makes this program the clear winner on total cost.

SBA 7(a): Flexibility Across Components

We utilize the SBA 7(a) loan as a general-purpose financing tool. The 2026 maximum loan limit for a standard 7(a) is $5 million. Our lenders prefer this option for complex restaurant startups because it funds multiple categories at once.

- Real estate purchases.

- Business acquisitions.

- Build-outs and equipment.

- Working capital reserves.

- Refinancing existing debt.

You can fund all these components under one unified package. We appreciate the single-lender structure because it simplifies the closing process. Variable interest rates are very common with this program.

Our current rate sheets show variable 7(a) rates tied to the Wall Street Journal Prime Rate. The Prime Rate sits at 6.75% as of mid-2026. We see maximum allowable rates capping out around 9.75% for loans over $350,000.

- Single-lender setup offers a faster process than the 504 program.

- Flexible funds cover daily operations, marketing, or inventory.

- Typical terms include 10 years for equipment and 25 years for real estate.

- Lenders often require a 10% down payment for business acquisitions.

- Startups must demonstrate a Debt Service Coverage Ratio (DSCR) of at least 1.25x.

A 7(a) loan often fits better than trying to force a mixed deal into a strict real-estate structure. Our team uses this program to support multi-unit expansions where each location requires different asset types.

When Each Wins in an SBA 7a vs 504 Restaurant Deal

A simple decision framework helps route your application. We evaluate your specific capital needs and the physical property requirements. The table below places the data side-by-side to make your choice easier.

| Factor | SBA 504 | SBA 7(a) |

|---|---|---|

| Best Use | Real estate is 70%+ of total deal | Mixed real estate, working capital, build-out |

| Occupancy | Strict 51% (existing) or 60% (new) | More flexible across mixed-use spaces |

| Working Capital | Not permitted for operations or inventory | Allowed and frequently included |

| Lender Structure | Two lenders (Bank + CDC) | Single lender simplicity |

You should pick the 504 program when you want long-term rate certainty on a heavy property piece. We strongly suggest the 7(a) program for multi-unit expansions where working capital is critical.

A Worked Example

An example brings these concepts to life. We can look at a realistic scenario for a North Carolina operator.

Imagine a buyer purchasing an existing restaurant for $1.5 million total. Our appraisal values the real estate at $900,000 and the business equipment at $600,000.

Option A: SBA 504 Focus

The buyer uses the 504 program strictly for the building purchase. We structure a $450,000 conventional bank loan and a $360,000 CDC loan.

The borrower brings a $90,000 down payment to close the $900,000 property transaction. We then must secure separate financing for the $600,000 business component. The blended interest rate on the property stays lower, but managing two separate loans takes effort.

Option B: SBA 7(a) Simplicity

We can package the entire $1.5 million under one 7(a) structure instead. The buyer enjoys a single lender, a single closing process, and streamlined documentation.

Our borrowers might accept a slightly higher variable rate on the real estate piece to gain this convenience. The right answer depends on the buyer’s tolerance for complexity and available cash on hand.

Combining 504 with Conventional Financing

We frequently combine the SBA 504 with conventional financing for larger acquisitions. A new SBA rule taking effect in July 2026 expands these opportunities significantly. Our eligible borrowers can now combine 7(a) and 504 loans for up to $10 million in SBA-backed funding.

Conventional banks also have no limit on their 50% portion of a 504 deal. We see total project sizes routinely exceed $20 million because the bank portion remains uncapped.

This multi-lender strategy works perfectly when rate optimization on a high-value property matters most. Our commercial lending partners coordinate this structure to maximize your purchasing power.

Documentation Differences

Federal regulations require thorough financial vetting to protect the government guarantee. We need substantial paperwork to underwrite either SBA program. The initial checklist applies to both loan types.

- Three years of personal and business tax returns.

- Current financial statements and balance sheets.

- Debt Service Coverage Ratio (DSCR) projections (see our DSCR guide).

- A comprehensive business plan or project narrative.

We must also collect real-estate-specific materials for the CDC. The 504 program requires these extra items:

- A certified commercial real estate appraisal.

- A Phase I Environmental Site Assessment (ESA).

- Detailed property condition reports.

- Specific application forms for the Certified Development Company.

We notice timelines remain comparable despite the extra paperwork. Standard closing timeframes range from 4 to 10 weeks depending on project complexity.

Next Step

We know that buying restaurant real estate is a massive commitment.

Deciding on an sba 7a vs 504 restaurant loan dictates your long-term monthly overhead. Our team is ready to review your exact property details and financial goals.

You can Pre-qualify online or call (910) 685-8872 to start the conversation. We will assess your deal mix and route you to the most profitable program.