Have you ever stared at a broken walk-in freezer on a Friday night, wondering how you will pay for the repair before the weekend rush?

We see independent restaurant owners use Merchant Cash Advances to solve this exact problem every single day. The kitchen breaks down, and you simply need money yesterday because cash flow problems cause over 82% of small business closures.

Our team at Restaurant Financing Pros NC will walk you through the details in a simple, step-by-step way.

Who an MCA Fits

Merchant cash advances are an excellent product for restaurants pulling in strong daily card sales. You might have a credit profile, short business history, or highly seasonal cash flow that makes standard loans difficult.

We step in when traditional banks say no. The U.S. Small Business Administration tightened their rules in early 2026, meaning standard bank loans now require full manual underwriting and weeks of waiting.

Why Standard Loans Fall Short

Standard loans focus heavily on your past credit history. An advance looks directly at your daily momentum instead.

We find this structure fits perfectly for several specific situations:

- Credit scores under 600: Traditional lenders typically reject these applications immediately.

- Startups under two years old: You have strong daily sales but lack the long track record banks demand.

- Deeply seasonal businesses: Your summer revenue in places like the Outer Banks dwarfs your winter numbers.

- Emergency repairs: You need cash in 24 hours to replace a dead walk-in cooler.

Many new operators use platforms like Square or Toast to process customer payments. These modern POS systems integrate perfectly with an advance structure.

Our underwriting team simply pulls a soft credit check, which will not hurt your score, and reviews three to six months of business bank statements. Same-day funding is incredibly common once your file clears.

How Repayment Works

Instead of demanding a fixed monthly payment, a cash advance relies on a small daily split of your credit card sales. This split is called the holdback percentage, or it might function as a daily ACH sweep from your business account. If you want the mechanics start to finish, our guide on how a restaurant merchant cash advance works breaks down every step.

Our merchants love this setup because the mechanics actually work in their favor. Your payment shrinks on a slow Tuesday, and it grows on a busy Saturday night.

This natural tracking makes it a perfect fit for seasonal operators. We see average holdback percentages sitting between 10% and 20% of daily sales across the U.S. in 2026. You never have to write a massive check when revenue dips.

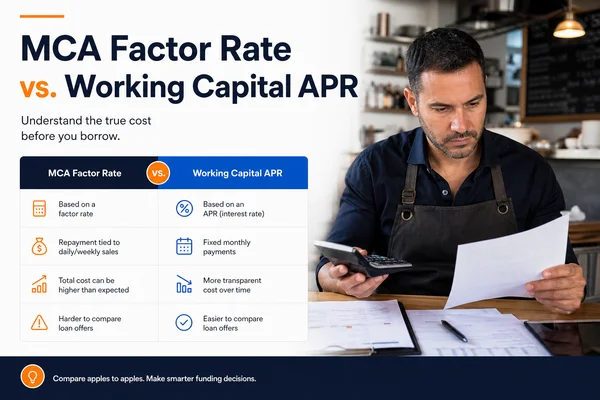

Understanding the Factor Rate

The cost structure looks very different from a traditional bank loan. Instead of an APR, an advance uses a fixed multiplier applied right at signing called a factor rate.

We want to make this math crystal clear. Average MCA factor rates currently sit between 1.10 and 1.55 in 2026, depending on your risk profile.

Here is exactly how the pricing works:

- Fixed Total Cost: A factor rate of 1.3 on a $50,000 advance equals a $65,000 total repayment.

- Locked-In Pricing: Our team locks this cost in stone at signing.

- No Interest Surprises: Early payoff offers no financial benefit, but you also never face any surprise accruing interest.

Transparency is critical when comparing your choices. We disclose the factor rate, the holdback percentage, and the total cost upfront. You will know the exact cost of the capital before you ever commit to a contract.

Merchant Cash Advance vs. Traditional Loan

Comparing your options side-by-side helps clarify the best path forward. Speed and flexibility define the advance, while low cost defines the loan.

We built this quick comparison table to highlight the major differences.

| Feature | Merchant Cash Advance | Traditional Bank Loan |

|---|---|---|

| Funding Speed | 24 to 48 hours | 4 to 8 weeks |

| Repayment Method | 10% to 20% of daily sales | Fixed monthly payment |

| Cost Structure | Fixed factor rate (1.10 - 1.55) | Annual Percentage Rate (APR) |

| Credit Requirement | Flexible (Sub-600 approved) | Strict (680+ typically required) |

When to Choose an MCA vs. a Working Capital Loan

Honest answer comes first. If you qualify for our restaurant working capital, that traditional route is almost always cheaper.

We require one year in business, $150,000 in yearly revenue, and a 600 credit score for that program. Cash advances trade a higher cost for incredible speed and approval flexibility.

Here are the signs that you need an advance instead:

- Low Credit: Your score currently sits below 600.

- Severe Seasonality: Your revenue swings wildly between seasons.

- Immediate Need: You require funding in your account today.

Standard loans often take weeks to process, but an advance can hit your account in 24 to 48 hours. Our advisors will openly discuss these details during your diagnosis call.

You will never be sold an advance if a better option exists for your kitchen. Sometimes, speed is your only lifeline, and Merchant Cash Advances provide the structure that works.

We always remain straight about the costs and the trade-offs involved. You deserve to make the final call with completely clear, full information.

“Our goal is to give you the exact numbers you need to make the right choice for your restaurant.”

Are you ready to explore your options?

We make the next step incredibly easy.

Pre-qualify in 60 seconds or call (910) 685-8872 right now.