The Acquisition Decision

We know that choosing between SBA vs conventional franchise financing shapes your entire growth trajectory.

Most buyers face this critical choice when taking over an existing location or launching a new unit. Fast-casual concepts run anywhere from $250,000 to over $750,000 in 2026, while full-service establishments easily push past the $1.5 million mark.

Our team has structured hundreds of these deals, and the right path always hinges on your specific timeline and cash flow needs. Franchise restaurant financing through our network handles both SBA and conventional routes perfectly. Let’s look at the current data and walk through the exact criteria you need to secure the best loan for franchise restaurant success.

SBA 7(a): The Conservative Path

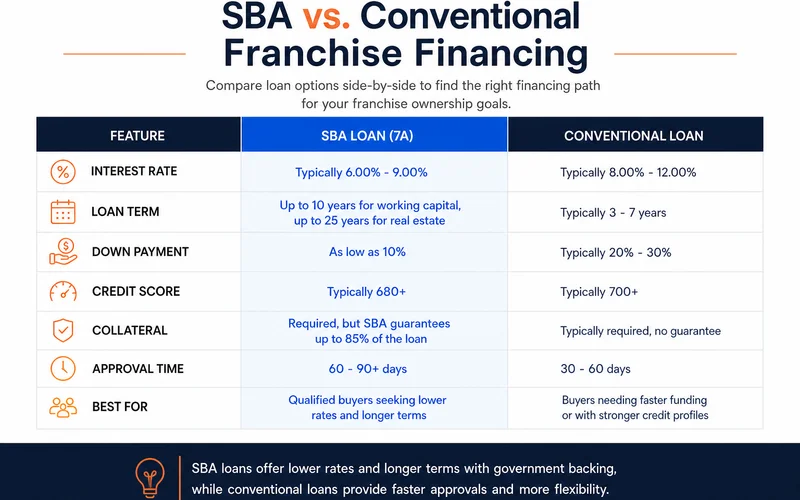

SBA 7(a) funding remains the most popular choice for substantial acquisitions in the United States. The Small Business Administration guarantees up to 85% of the loan for the lender. This heavy federal backing translates to highly favorable terms for independent operators here in North Carolina and across the country.

We regularly recommend the SBA 7(a) program when your deal size exceeds $500,000. Interest rates for variable 7(a) loans are capped by the government, hovering between 9% and 11.5% in mid-2026 with the Prime Rate at 6.75%. That cap provides a serious shield against runaway borrowing costs.

Ideal Scenarios for SBA Financing

A conservative approach fits best under specific conditions. You will find the highest success rates when your situation matches these factors:

- Deal size is meaningful: The project requires $500,000 up to the $5 million program maximum.

- Long-term rate matters more than speed: You can afford a 60-day to 90-day wait.

- The franchisor is SBA-friendly: Most major systems maintain a strong presence on the SBA Franchise Directory.

- Documentation is pristine: You have three years of tax returns, clean financial statements, and a solid business plan ready.

Recent Policy Advantages

The agency actually removed the mandatory FICO SBSS minimum score of 165 for small loans under $350,000 in March 2026. Lenders now have more flexibility to use their internal scoring models. You also benefit from repayment periods stretching up to 10 years for equipment and 25 years for real estate.

Our clients love that SBA packages often roll the working capital reserve directly into the funded amount. A major trade-off is the paperwork burden and the strict Debt Service Coverage Ratio underwriting. You need to clear a 1.15 minimum DSCR, though most lenders prefer to see 1.25 or higher before issuing an approval.

Conventional: The Speed Path

Conventional franchise financing strips away the federal red tape to get your doors open faster. Regional banks and specialized commercial lenders fund these deals directly out of their own portfolios. You can typically secure funding in two to four weeks instead of the two months required for government-backed options.

We lean on conventional lending heavily when franchisors like Firehouse Subs or Smoothie King push for a tight opening schedule. Commercial loan rates in 2026 generally start around 7% for highly qualified borrowers, stretching past 10% depending on the asset risk. You pay a premium for speed, but missing a grand opening deadline costs far more in lost revenue.

When to Choose Commercial Lenders

This faster route makes the most sense for operators facing specific constraints. Consider a conventional commercial loan if you hit these criteria:

- Timeline is tight: You have a hard closing date or intense franchisor pressure.

- Deal size is smaller: The acquisition cost does not justify the massive paperwork burden.

- Your file has a marginal SBA fit: Your credit sits in the mid-tier range, or your DSCR is borderline.

- You want flexible structures: You need customized terms that standardized government programs reject.

The Trade-Offs of Speed

Our lending partners process these files quickly because they require less documentation and coordinate directly with the franchisor. However, conventional term lengths usually cap out at 5 to 10 years. A shorter amortization schedule forces your monthly payments significantly higher.

You might also have to fund your working capital reserve through a separate line of credit rather than wrapping it into the main note. Some franchise systems do mandate their own preferred conventional lenders. Those mandated choices may not always offer the most competitive terms for your specific financial profile.

A Cost Comparison

Evaluating a $1 million franchise acquisition requires looking at the math side-by-side. The total interest paid over the life of the loan often surprises first-time buyers.

We built this comparison using typical 2026 market rates to show how the term length dictates your cash flow. A longer runway drastically reduces your monthly burden.

Side-by-Side Financial Breakdown

| Loan Feature | SBA 7(a) Loan | Conventional Loan |

|---|---|---|

| Term Length | 10 Years | 7 Years |

| Interest Rate | 9% | 13% |

| Monthly Payment | approx. $12,670 | approx. $18,180 |

| Total Interest Paid | approx. $520,000 | approx. $527,000 |

| Total Cost | approx. $1.52 Million | approx. $1.53 Million |

The data reveals a surprisingly similar total cost in this specific scenario. The monthly payment difference of $5,510 is the real deciding factor. SBA’s longer term creates lower monthly debt service obligations.

That lower payment means stronger DSCR coverage post-acquisition, giving your restaurant breathing room during the critical first year. Most franchise operators care far more about comfortable monthly cash flow than a modest difference in total interest over a decade.

Combining Both

Large franchise acquisitions frequently benefit from a dual-lender strategy. Blending both financing types gives you the long-term stability of government backing with the rapid deployment of commercial capital.

We coordinate this two-lender structure to keep your project moving while the primary loan crawls through underwriting. The SBA file processes in parallel with the conventional closing. This ensures your heavy equipment installs right on schedule.

How the Split Works

Dividing the project costs into two distinct buckets maximizes your capital efficiency. Here is how the pieces fall into place:

- SBA covers the long-term assets: This includes the business value, goodwill, real estate, and your working capital reserve. You get the lower rate and the 10-year to 25-year term.

- Conventional covers the fast-deploy needs: This funds your kitchen equipment, furniture, fixtures, and opening inventory. The capital arrives in weeks instead of months.

Our team deploys this approach so operators never miss a franchise development timeline. Getting the kitchen built out while waiting on the final real estate paperwork saves massive headaches.

DSCR Considerations

Debt Service Coverage Ratio measures your restaurant’s cash flow against its proposed debt obligations. Both government and private lenders use this metric as the primary pass or fail test for your application.

We scrutinize your DSCR before submitting any file to an underwriter. The calculation takes your net operating income and divides it by the total annual debt payments. A ratio of 1.0 means you make exactly enough to pay the loan, leaving zero margin for error.

Benchmark Requirements

Different programs carry distinct baseline requirements for approval. Here are the typical 2026 thresholds:

- SBA Minimums: 1.15 is the hard floor, though underwriters heavily prefer 1.25 or higher.

- Conventional Minimums: 1.10 is sometimes acceptable, with 1.20+ preferred by regional banks.

Private lenders offer more flexibility at lower DSCR levels if you pledge stronger collateral. Underwriters calculate this ratio for franchise acquisitions using the target restaurant’s historical performance plus substantiated operational improvements. They also pull operating benchmarks directly from Item 19 of the franchisor’s Franchise Disclosure Document.

Review our DSCR guide to master the exact formula lenders use to evaluate your business.

What Most Franchisors Prefer

Most major national brands actively steer their franchisees toward government-backed financing. Established systems like Huddle House and Jack in the Box have dedicated internal finance teams built to handle this exact paperwork.

Our experience shows that recognizable brands maintain established relationships with preferred SBA lenders. This cuts weeks off the approval process because the bank already understands the restaurant model.

The Comfort Letter Requirement

A crucial piece of this puzzle is the franchisor comfort letter. This document gives the bank permission to take over and operate the location, or sell it to an approved buyer, if you default on the note.

- Standard Templates: Major brands keep pre-approved comfort letters ready to deploy instantly.

- SBA Directory: Brands listed on the official registry face fewer underwriting hurdles.

- Direct Coordination: Corporate finance teams speak directly with underwriters to clear up unit-level economic questions.

When Corporate Pushes Private Capital

Smaller or emerging concepts often lack the historical data required for government approval. A conventional commercial loan is usually required for newer franchise models with limited track records.

Brands will also point you toward private capital if your acquisition timeline simply cannot accommodate a 60-day underwriting delay. Buyers with marginal credit scores often find a smoother approval process going straight to a commercial bank.

The Diagnosis Call

Finding the perfect capital structure does not require endless web research or blind applications. The fastest way to determine your best path is a simple pre-qualification review.

We conduct a detailed diagnosis to match your specific restaurant project with the right capital source immediately. This upfront analysis handles the complex math so you can focus on running the kitchen.

The Five-Point Assessment

During our initial consultation, the evaluation covers the critical factors that dictate lender appetite. We specifically diagnose these five areas:

- Deal size and structure: Total capital needed and asset breakdown.

- Your credit and DSCR profile: Personal financial strength and business cash flow.

- Timeline pressure: Hard deadlines from the seller or corporate office.

- Franchisor preferences: Existing brand relationships with specific banks.

- Real estate split: The ratio of property value compared to business-only assets.

The resulting recommendation points you toward an SBA loan, a conventional product, or a strategic combination of both. We then route your file directly to the right lender from the very start, eliminating wasted time. This immediate routing protects your acquisition timeline.

Next Step

Acquiring a new location represents a massive leap for your business. You need a financing partner who understands the fast-paced realities of the hospitality industry.

Our funding specialists are ready to review your deal sheet today. Pre-qualify online or call (910) 685-8872 to walk through a complete diagnosis of your franchise acquisition loan options.