Our team talks with independent restaurant owner-operators every single week about funding their next location. Finding the right physical space is just the first hurdle.

The real challenge is securing the capital to transform that raw square footage into a functional kitchen and dining room before your rent abatement runs out. If you are starting from a bare shell, our restaurant build-out from shell space guide walks through what that financing covers and how funding is phased.

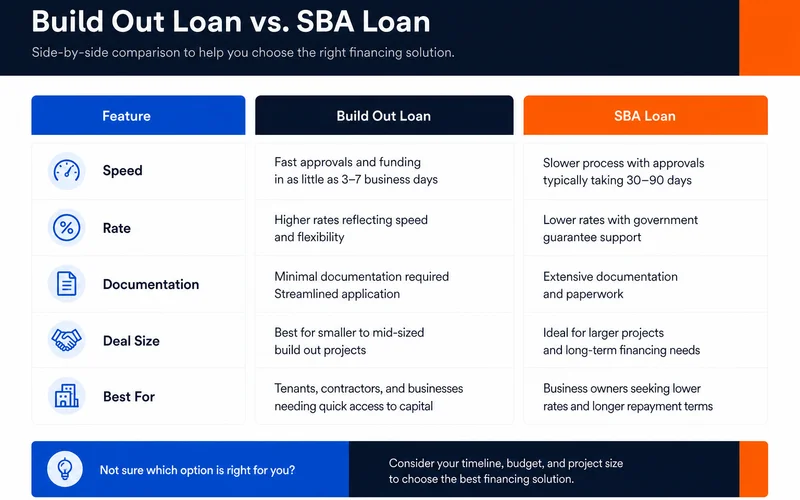

For most NC restaurant operators considering a major remodel or shell-space build-out, the choice between conventional build-out financing and an SBA 7(a) loan comes down to a familiar trade-off. You are balancing speed and flexibility against rate and term length.

We will break down exactly how these two options compare based on current market data.

The Core Trade-Off: Speed vs. Rate

Our clients constantly ask about the restaurant build out loan vs sba comparison. As of mid-2026, the average cost for a full-service restaurant build-out in the US sits between $350 and $550 per square foot. Funding a 2,000-square-foot space requires serious capital.

A simple framing clarifies the decision:

- Build-out financing closes fast within a few weeks and accommodates flexible structures. It carries higher interest rates than SBA options.

- SBA 7(a) financing offers lower rates and longer repayment terms. This route takes four to eight weeks to close and requires substantially more documentation.

Neither path is universally right. The correct structure depends on your timeline, the total deal size, and how much of the project can wait for the formal underwriting process.

When Build-Out Financing Wins

Conventional build-out financing tends to be the preferred choice in several specific scenarios.

- Timeline is tight. You have a lease signed, contractors mobilizing, and equipment lead times that cannot wait for SBA underwriting.

- Deal size is moderate. Projects under $300,000 often do not justify the heavy documentation burden.

- You are refreshing rather than transforming. A dining room refresh or replacing a broken Rational combi-oven fits this model cleanly.

- You will refinance later. Some operators use this fast capital to open quickly and refinance into an SBA product once they build a post-opening operating history.

Our data shows that equipment financing approvals often happen in 24 to 48 hours. The rates are higher than government-backed loans. That premium easily pays for itself when fast deployment gets your doors open weeks earlier and starts generating revenue.

When SBA 7(a) Wins

The sba vs conventional build out debate shifts in favor of the government program for larger, more permanent investments.

- Deal size is large. The SBA caps variable interest rates based on loan size. In 2026, loans over $350,000 benefit from the lowest margin cap of Prime plus 3.0 percent, making the rate savings highly attractive.

- You have time. A four to eight week underwriting window aligns perfectly with your construction schedule.

- You are acquiring real estate. The 7(a) program or a 504 loan is the definitive tool when a property purchase is part of the project.

- Cash-flow sensitivity is high. Longer repayment periods spanning 10 to 25 years keep your monthly debt service manageable.

We frequently recommend this path for massive overhauls where construction sequencing takes months anyway. The significant rate advantage easily justifies the extra paperwork required upfront.

Why Combining Both Often Wins for Big Projects

For projects exceeding $500,000, the smartest restaurant remodel financing options usually involve combining both structures. You do not have to pick just one.

Our preferred arrangement splits the capital needs into two distinct tracks.

- SBA 7(a) covers the construction shell, structural changes, and long-horizon capital needs. This secures a lower rate over a longer term.

- Build-out financing covers the furniture, fixtures, and immediate equipment purchases like your Toast POS system or walk-in cooler. This provides faster funding directly to your vendors.

This hybrid approach allows you to open on time without stalling your equipment orders. The government loan file runs in parallel with your physical construction work. Your necessary equipment funds quickly, installs on schedule, and your kitchen is ready to operate.

We coordinate these two financing tracks carefully so they never conflict.

A Data-Driven Comparison

Understanding the exact differences helps you plan your cash flow effectively. Here is a clear look at how the two primary funding types stack up in 2026.

| Feature | Conventional Build-Out | SBA 7(a) Loan ($350K+) |

|---|---|---|

| Typical Closing Time | 2 to 7 days | 30 to 60 days |

| 2026 Interest Rate | 10% to 25%+ (Risk-based) | Approx. 9.75% (Variable cap) |

| Repayment Term | 2 to 5 years | 10 to 25 years |

| Primary Collateral | The equipment itself | Business assets, personal guarantees |

Documentation Comparison

A quick view of what each path requires reveals a significant difference in administrative workload.

Conventional build-out financing:

- 60-second pre-qual (soft credit pull)

- 3 months business bank statements

- Construction contract and contractor information

- Equipment invoices and vendor list

- Basic business information

SBA 7(a):

- All of the above basic requirements

- 3 years of business and personal tax returns

- Detailed financial statements including a balance sheet and profit and loss statement

- Business plan or detailed project narrative

- Debt service coverage ratio projections showing a minimum of 1.15x

- Personal financial statements for all owners

- Real estate documentation if applicable

- Construction draw schedule

Our underwriting team sees this documentation gap constantly. The rigorous government process is appropriate for massive deals, but it feels overwhelmingly heavy for smaller kitchen updates.

A Worked Example

Let us look at a practical application using a $700,000 remodel project in Greensboro. The budget includes $300,000 for structural work and HVAC upgrades, $200,000 for kitchen equipment, and $200,000 for dining room finishes.

The operator chooses a blended approach to maximize efficiency. They utilize the 7(a) program for $400,000 to cover the structural work and half the heavy equipment at a lower rate over a 10-year term. They then secure conventional build-out financing for the remaining $300,000 to cover front-of-house finishes and the fast-arriving equipment.

“Securing the equipment fast with a conventional short-term note allows the kitchen to open on time, while the SBA loan provides long-term stability for the massive structural costs.”

Our preferred strategy allows the physical assets to arrive and install precisely on schedule. The longer-term loan closes mid-project, providing favorable rate benefits for the large expenses.

This represents a typical and highly effective structure for North Carolina startups.

Next Step

Sizing a remodel or build-out requires careful planning. Do you need to talk through these structure trade-offs?

We can help you evaluate your specific timeline and budget.

Pre-qualify in 60 seconds or call (910) 685-8872 to discuss the right path for your project.