You know how the final stages of opening a restaurant always seem to require more cash than planned.

From what I’ve seen, managing the soft costs right at the end is what separates a smooth launch from a stressful scramble. Our team fields questions about ffe financing restaurant structures every single day. This specific funding is a critical tool for preserving your working capital just before opening day.

Let’s look at the data, what it actually means for your budget, and explore a few practical ways to respond. I am going to break down the main reasons lenders treat this category differently and then walk through the exact funding structures that keep projects on schedule.

What FF&E Actually Covers

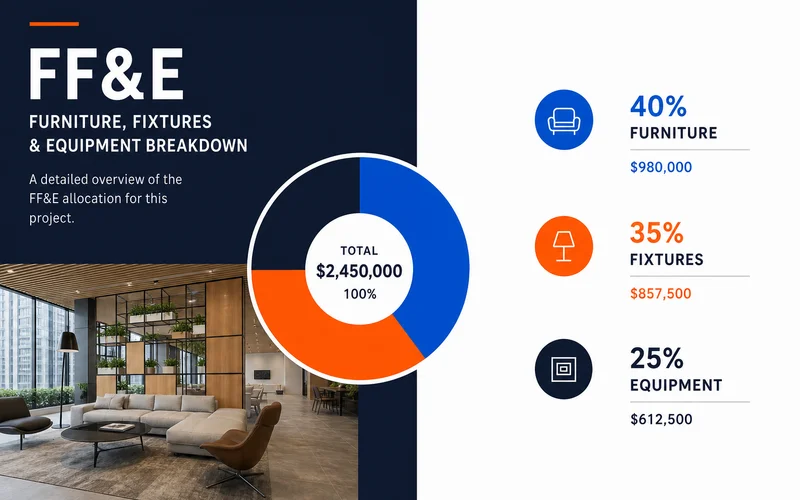

FF&E stands for Furniture, Fixtures, and Equipment, which is the broad category covering everything that fills a restaurant beyond the building shell itself. This classification includes the dining room tables, the kitchen hoods, and the POS systems that make your operation run.

Our clients often confuse this with standard equipment financing, but the scope is much wider. The major difference is that FF&E includes the front-of-house elements that pure equipment loans typically reject. For a typical restaurant build-out, this breaks down into three distinct areas.

Furniture:

- Dining tables and commercial-grade chairs

- Booths and banquettes

- Bar stools

- Host stand and waiting-area seating

- Outdoor patio setups

Fixtures:

- General, accent, and decorative lighting

- Bar tops and custom back-bar shelving

- Built-in storage and wait-station counters

- Window treatments

- Decorative wall elements

Equipment:

- Commercial kitchen ranges and hoods

- Bar ice wells and glassware coolers

- POS hardware like Toast or Square terminals

- Refrigeration units from brands like True

- Commercial dishwashing systems

Handling a major project from scratch? Build-out and remodel financing can wrap the full FF&E package into a single build-out deal, or you can fund it separately if the construction is already handled.

Why FF&E Financing Exists As a Category

A typical commercial equipment loan focuses on heavy gear like walk-in coolers and heavy-duty Vulcan ranges. These assets hold their value for a decade or more, making them strong collateral. Our lending partners view soft assets very differently. Pure equipment financing often skips dining-room chairs, decorative lighting, and bar fixtures because they depreciate much faster and have significantly lower resale value.

Industry data shows a commercial dining chair undergoes over 250,000 stress cycles and needs replacing every five to ten years. Lenders created the furniture fixtures equipment financing category to bridge this exact gap. It covers these softer items, often using a 24 to 60-month lease structure that perfectly matches their faster depreciation timeline.

Bundling Into a Build-Out

For shell-space build-outs and major renovations, the cleanest path is to roll everything into the main project loan. This approach gives you one unified financing structure covering the entire scope of work. We usually recommend this route to keep paperwork simple. A single closing provides one payment and one coordinated timeline.

Current 2026 data shows the average U.S. restaurant build-out takes anywhere from 6 to 14 months from planning to opening. Managing multiple loans during that long stretch creates unnecessary administrative headaches. This single structure covers:

- Core construction

- Custom fixtures

- Dining room FF&E

- Heavy kitchen equipment

Tranches release on construction milestones, a process discussed in our build-out guide.

Standalone FF&E Financing

If your primary construction is already funded, you can secure a restaurant ffe loan as a separate package. An SBA 7(a) loan might cover the shell improvements, leaving the interior finishes for a standalone deal. We see this split-funding strategy used frequently to protect working capital for the first few months of payroll. The structure looks exactly like standard equipment financing, just with broader coverage for those front-of-house items.

Lease structures are incredibly common here because they accommodate the diverse depreciation profiles across different assets. A 36-month lease handles the rapid wear and tear on bar stools perfectly. This shorter term prevents you from paying for seating long after it has been thrown away.

Cost Ranges

FF&E budgets vary widely by concept, square footage, and the quality of finishes chosen. Recent 2026 construction data shows full-service dining build-outs regularly hit $350 to $550 per square foot. Our team uses these baseline figures to help new operators set realistic expectations. Kitchen equipment alone easily consumes 50 to 70 percent of this budget.

Typical 2026 Budget Estimates

To help you plan, here is a breakdown of total costs excluding the building shell construction.

| Restaurant Concept | Estimated Total FF&E Cost |

|---|---|

| Casual quick-service | $50,000 to $120,000 |

| Mid-tier full-service | $120,000 to $250,000 |

| Upscale or premium | $250,000 to $500,000 |

| High-end fine dining | $500,000 and up |

These numbers account for current inflation and supply chain realities. Sourcing commercial-grade materials upfront saves significant money on replacements later.

Ownership and End-of-Term

The end-of-term options function exactly the same as a standard equipment lease. The structure you choose directly dictates your tax benefits and ownership rights. We always suggest reviewing these options with your CPA before signing.

- EFA structure: You own the items from day one, while the lender simply holds a lien.

- Equipment loan: Similar to an EFA, you retain ownership and the lender holds a lien.

- Capital lease: You gain tax treatment similar to outright ownership.

- Operating lease: The lessor retains the title, and you expense the monthly payments.

The tax advantages for purchasing business equipment are massive right now. The IRS set the 2026 Section 179 deduction limit at $2,560,000, and bonus depreciation is currently at 100 percent. See our Section 179 guide for specific tax treatment details on each of these financing structures.

A Worked Example

A mid-tier restaurant in Charlotte with a $400,000 total project budget requires a strategic mix of capital. A typical breakdown might allocate $180,000 for construction, $90,000 for kitchen appliances, and $130,000 for front-of-house furnishings. Our specialists regularly coordinate these multi-tiered funding packages for North Carolina operators. The construction phase is financed via an SBA loan, the kitchen gear uses an EFA, and the remaining items are covered by a lease.

These three pieces close in different structures but stay perfectly synchronized. This coordinated timeline ensures your grand opening happens on schedule. That is the standard approach for a larger build. For smaller projects under $200,000 total, the entire package often fits into a single, unified approval alongside the heavy equipment.

Next Step

Sizing your budget for a brand new build-out or a dining room refresh? Prequalifying takes the guesswork out of your planning phase. We can review your specific needs and outline your exact borrowing power today. Pre-qualify in 60 seconds or call (910) 685-8872 to walk through the right structure.