We constantly see independent restaurant operators hit a wall when pricing out their first commercial kitchen build.

Founders often experience sticker shock as the median startup cost for an independent US restaurant has climbed to $375,000 in 2026.

That is a massive financial hurdle for any new local business.

Our team wrote this guide to clarify the options on the table.

Comparing an equipment finance agreement vs lease restaurant structure dictates your tax strategy and daily cash flow. Because the structure you pick also shapes your deduction, our Section 179 and tax treatment guide is worth a read alongside this one.

You need to understand these critical differences before applying for restaurant equipment financing.

The Three Structures, Plain English

You will typically encounter three distinct funding models for your North Carolina kitchen, and they all allow you to acquire essential gear without draining your operating cash.

Our goal is to help you distinguish between the financial mechanics of each choice.

The core differences center around asset ownership, tax deductions, and end-of-term obligations.

- Ownership status: Who holds the legal title to the asset.

- Tax treatment: How the IRS views the monthly payments and depreciation.

- End-of-term action: What happens after you make the final payment.

We find that understanding these three pillars makes the final decision obvious.

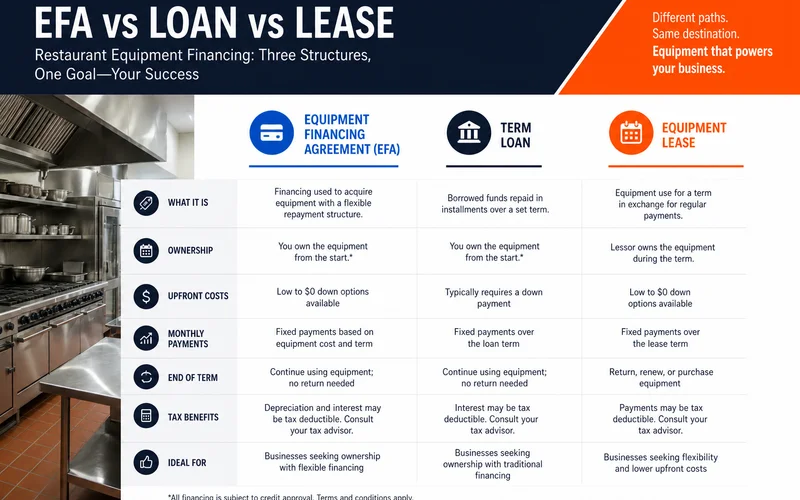

EFA, Equipment Finance Agreement

An EFA restaurant financing arrangement functions as a hybrid between a traditional loan and a standard lease.

You hold the official title to the asset from the very first day of delivery.

Our financing partners simply file a UCC-1 lien against the specific item until the balance clears.

Monthly payments mirror a standard amortization schedule.

This keeps your cash flow highly predictable.

Because you retain ownership, you get to claim depreciation on your federal tax return.

The tax advantages are massive for independent operators right now.

Our CPAs remind clients that the 2026 Section 179 deduction limit jumped to $2.56 million.

The recent One Big Beautiful Bill Act (OBBBA) restored bonus depreciation to 100% for 2026.

This means a restaurant spending $100,000 on a kitchen upgrade can potentially deduct the entire amount in year one.

EFAs are generally the strongest fit for operators who:

- Want immediate ownership and the massive 2026 tax depreciation benefits

- Intend to run the specific hardware well past the financed term

- Prefer a structure that sits on the balance sheet like a traditional loan

Simple-Interest Equipment Loan

This is the most traditional borrowing method for securing capital assets.

You take out a specific principal amount, pay a fixed interest rate, and the lender holds the lien.

Our data shows good-credit operators are currently securing 2026 interest rates ranging from 7% to 12% APR.

Interest accrues only on the remaining principal balance.

Paying the balance down early directly reduces the total interest you owe.

Loan Requirements and Terms

Borrowers with pristine credit histories frequently qualify for zero-down funding.

Startups or those with lower credit scores usually need to provide a 10% to 20% down payment.

We generally see repayment terms spanning three to seven years for heavy-duty commercial appliances.

For massive multi-million dollar buildouts, some operators utilize SBA 7(a) loans.

These government-backed loans have variable rates capped around 9.75% for larger amounts this year.

Traditional loans work best for owners who:

- Have excellent credit and want straightforward, predictable terms

- Value the flexibility to make early payments without severe penalties

- Do not require the specialized tax mechanics of an EFA or lease

Lease

A commercial lease leaves the legal title with the financing company.

You simply pay a monthly fee to utilize the hardware inside your kitchen.

Our clients typically choose between a $1 buyout option or returning the gear at the end of the term.

Accounting rules divide these into operating leases and capital leases.

Operating leases are kept off the balance sheet, while capital leases are recorded differently.

The Bundling Advantage

The primary benefit for a fast-paced restaurant is the ability to bundle soft costs.

Lenders allow you to wrap freight delivery, installation labor, and software licenses into a single monthly payment.

We cannot easily do this with a standard loan, which usually only covers the physical metal.

Technology Refresh Cycles

Commercial-grade POS hardware generally has a lifespan of just five to seven years.

Consumer tablets used for tableside ordering often burn out in three to five years.

Our team recommends leasing for these rapid-depreciation items so you avoid holding obsolete technology.

At the end of the lease, you simply trade up to the newest software and hardware package.

Leases tend to fit operators who:

- Need lower monthly payments to preserve operational cash flow

- Require software, installation, or service contracts bundled in

- Plan to cycle out fast-aging technology like POS registers frequently

- Have specific tax preferences requiring an operating lease structure

How to Pick

Choosing between an equipment finance agreement vs lease restaurant structure boils down to your primary business goals.

Comparing a restaurant equipment loan vs lease requires looking closely at your long-term plans.

We created a quick decision matrix to simplify your choice.

| Your Primary Goal | Best Structure | Why It Works Best |

|---|---|---|

| Max Tax Write-Offs | EFA | Unlocks full 2026 Section 179 and 100% bonus depreciation. |

| Lowest Overall Cost | Equipment Loan | Simple interest allows you to pay early and save money. |

| Bundled Soft Costs | Lease | Wraps freight, installation, and software into one payment. |

| Frequent Tech Upgrades | Lease | Prevents getting stuck with obsolete 5-year-old POS tablets. |

| Long-Term Utility | EFA or Loan | Best for 10-year assets like walk-in coolers and heavy ranges. |

A few universal rules apply to every scenario.

Your personal credit profile heavily influences your approval odds and final interest rate.

We notice that the expected useful life of the gear must always align with your contract length.

Talk to your CPA

Tax codes change rapidly, and the massive 2026 Section 179 expansion alters the math for profitable restaurants. The right choice depends entirely on your current corporate structure and taxable income. We specialize in funding the gear, but your CPA must verify how each structure fits your tax picture before you sign.

Common Trade-Offs

Every financial product carries specific advantages and disadvantages.

Choosing the wrong setup can strain your monthly operating budget.

Our financing specialists see operators struggle with a few recurring themes.

Cash Flow Versus Total Expense

Protecting your daily cash flow is the most important survival tactic for a young restaurant.

Well-qualified borrowers can score zero-down loans, keeping cash in the bank for payroll and food orders.

We know that leases sometimes cost slightly more over the long run due to the lender carrying the residual risk.

That said, the lack of a massive upfront down payment often makes the lease mathematically superior for startups.

End of Term Realities

You must plan for the final month of the contract before you sign the first page.

Loans and EFAs result in clear, undisputed ownership once the final check clears.

Our lease contracts require you to make an active choice between buying the asset, returning it, or extending the rental period.

Failing to exercise a lease option on time can trigger automatic, expensive monthly renewals.

You must track these dates closely to avoid surprise charges.

Next Step

Finding the exact right equipment finance agreement vs lease restaurant deal takes just a few minutes.

Our 60-second process reviews your credit, the desired asset, and your timeline to match you with the perfect product.

Pre-qualify in 60 seconds or call (910) 685-8872 to get started.