Restaurant Financing Pros NC helps North Carolina restaurant owners get the equipment and working capital they need to open, expand, and stay competitive. Getting a bank turndown restaurant equipment loan application feels like a closed door.

The reality is that traditional lending models penalize the hospitality industry.

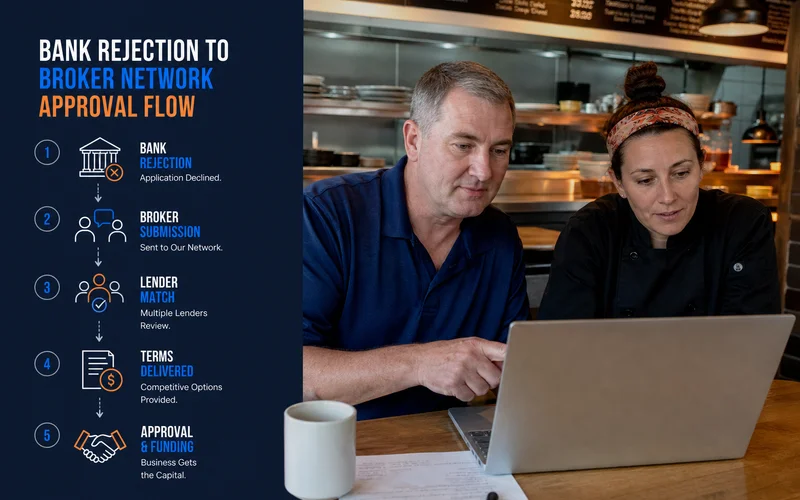

Profitable businesses fail the bank test every day because of strict debt service coverage ratios or short operating histories. Our restaurant equipment financing works differently by stepping outside those narrow criteria. A simple shift in underwriting strategy turns a rejection into a funded kitchen.

This guide explains the exact reasons behind bank denials and outlines a faster path to approval. Let’s look at the data to see what causes these rejections and explore the exact steps to bypass the bank entirely.

Why Banks Decline Restaurant Deals

Banks decline restaurant deals because their underwriting templates penalize the hospitality sector for perceived industry risks, tight cash flow metrics, and short business histories. A traditional institution often rejects a profitable operation, resulting in a bank turndown restaurant equipment loan simply because the file falls short on one specific metric.

Most traditional lenders enforce a strict Debt Service Coverage Ratio of 1.25x. This means your business must generate $1.25 in net operating income for every dollar of debt payment. A solid operation often fails this test because of existing debts. Another major hurdle is the credit score requirement. Conventional banks usually demand a FICO score of 680 or higher. A temporary credit dip from a tough season instantly disqualifies an otherwise healthy application, which is exactly the situation our bad-credit restaurant equipment financing guide is built to address.

- Time in business: Most banks require two or more years of operating history with consistent revenue.

- Credit profile: A recent credit dip drops you below the 680 FICO threshold.

- Industry risk: A famous UC Berkeley study shows only 17 percent of restaurants fail in their first year. Institutions still model restaurants as high-failure-rate industries and require larger margins of safety.

- Deal type: Used equipment, food trucks, and unconventional structures fall outside many rigid product lines.

- One-size underwriting: Banks usually evaluate a denied business loan restaurant file against a single strict template.

We match your deal to lenders in a network instead of relying on one bank’s narrow criteria. Different lenders specialize in different tiers and structures. Files that fail at Lender A often fit cleanly at Lender B.

What Broker/Network Underwriting Looks Like

Broker and network underwriting replaces a single rigid bank policy with multiple specialized funding options adapted to your specific deal. This approach matches your unique credit tier and equipment needs to the exact lender most likely to approve it.

Our network approach changes the fundamental rules when you bring us a turndown deal.

Commercial kitchen setup costs in 2026 average between $40,000 and $200,000. A traditional bank struggles to finance these specific asset amounts without broad guarantees.

Here is how the structure adapts:

- The underwriter changes: The file goes directly to a lender whose criteria fit your exact credit tier, time in business, and equipment type.

- The structure changes: A bank might try to write a rigid 5-year term loan. The new structure could be a 4-year Equipment Finance Agreement with a customized rate.

- The collateral framing changes: Banks demand broad business and personal guarantees. Equipment financing secures the loan against the specific assets using a standard UCC-1 filing in North Carolina.

- The down payment changes: Banks offer minimal down payments but require flawless credit histories. The alternative structure might take a larger down payment to grant approval access at thinner credit tiers.

The 3-Minute Phone Diagnosis

The fastest way to find out if your business qualifies for alternative funding is a brief phone call. Three minutes provides enough time to identify the exact reason for the bank rejection and match your file to a willing underwriter.

We can quickly determine your best path forward during a short consultation.

A typical bank SBA loan application requires weeks of waiting just to get a preliminary answer. This initial phone assessment skips the delays and gets straight to the facts. In three minutes the process will:

- Diagnose the bank turndown reason: The team identifies if the issue was a low Experian credit score, short operating history, or an unconventional deal type.

- Match the file to a likely lender: The diagnosis points directly to the right underwriter in the financing network.

- Provide an honest assessment: Sometimes a deal cannot be funded immediately. The representative will state this clearly rather than wasting valuable time.

Our next step for eligible files is a 60-second soft-pull pre-qualification. This soft pull checks Dun & Bradstreet and consumer credit bureaus without impacting your score. You receive a realistic read on the approval and structure before committing to a full application.

| Feature | Bank Process | Network Diagnosis |

|---|---|---|

| Initial Read | Weeks of underwriting | 3 Minutes |

| Credit Check | Hard inquiry | 60-Second soft pull |

| Flexibility | Single rigid criteria | Multiple network lenders |

What to Have Ready When You Call

Having your basic financial details and equipment lists prepared before dialing ensures a faster and more accurate funding diagnosis. Gathering specific numbers allows the team to pinpoint exactly which underwriter fits your current profile.

We need a few specific pieces of information to evaluate your options efficiently. Access to accurate numbers prevents delays in the pre-qualification stage. You should compile the following items before picking up the phone:

- The bank’s decline reason: Share the exact feedback if the institution provided it.

- The specific equipment list: Detail the items needed, such as a $15,000 combi oven or a walk-in cooler, and the approximate deal size.

- Your rough credit tier: The representative will perform a soft pull for exact Experian or Equifax figures later.

- Financial health metrics: Provide your time in business, rough annual revenue, and current net operating income to check your debt service coverage ratio.

A typical turndown call takes three minutes on the phone. The representative provides a same-day soft-pull pre-qualification and an honest read on approval probability. You decide whether to proceed with zero pressure.

Our firm operates without offshore call centers or automated phone trees. Clients get direct access to people who understand how to fund complex hospitality deals.

When We Can’t Help

A small percentage of turndown files simply lack both the necessary credit profile and the minimum equipment collateral value required for approval. Weak credit combined with fast-depreciating assets creates a risk profile that most equipment lenders cannot support.

We are completely transparent when a deal does not qualify for equipment financing. A sub-prime borrower attempting to finance an aging, used POS system usually faces a denial. These older electronics lose value immediately and offer terrible collateral for any lender.

“If a FICO score sits below 600 and the collateral holds minimal resale value, standard equipment financing is rarely the correct solution.”

Our specialists often suggest other financial paths for these specific scenarios. A merchant cash advance frequently serves as a better fit when monthly revenue is strong but traditional credit is thin. This alternative uses your daily sales volume instead of relying on equipment value.

Direct Access, Not Call Centers

Bypassing corporate call centers ensures you speak directly to the financial professionals handling your specific file. Direct access eliminates frustrating transfer queues and generic email responses that delay your funding process.

Our clients consistently highlight this personal approach as the biggest difference between this service and a traditional bank. You talk to the exact same team from the very first phone call until the kitchen equipment is fully funded. The process involves zero transfers between departments and zero escalation queues.

Large institutions commonly force applicants to wait five to seven business days just for a simple status update on an application.

We process information locally to provide answers in hours instead of weeks. This localized focus as an alternative restaurant lender nc keeps the process moving quickly. Direct communication remains the primary reason turndown clients express a wish they had called this office first.

Next Step

Rejection from a traditional institution does not mean your business concept is flawed or unfundable. Taking quick action to explore alternative underwriting networks can turn a bank turndown restaurant equipment loan into the necessary capital to move your project forward.

We encourage you to make one phone call before abandoning your equipment upgrade plans. The initial check involves a 60-second pre-qual with a simple soft pull. This step causes absolutely zero impact on your existing consumer credit score.

Reach out to the Wilmington office directly at (910) 685-8872 to start the conversation today.