The Core Mechanics

We understand how challenging it is to secure fast funding for an independent restaurant.

According to 2026 US Census Bureau data, roughly 60% of American restaurants are small businesses with fewer than 20 employees. These local shops often struggle to get traditional bank approvals quickly.

Our team regularly helps North Carolina operators compare alternative structures against standard loans.

A restaurant merchant cash advance explained simply is the sale of your future credit card receipts for an upfront lump sum. This means you get cash today without committing to a fixed monthly payment schedule.

Our priority is making sure you understand the math before signing anything.

For a direct breakdown of how this compares to other options, review our MCA vs. working capital loan guide. You can also explore the basic requirements in our main merchant cash advance hub.

We will walk through the exact mechanics right now.

Factor Rate vs. Interest Rate

A factor rate is a fixed multiplier applied to your funding amount at signing, whereas an interest rate accrues over time based on your remaining principal balance. This distinction is the single biggest source of confusion for new operators.

Our financing specialists always emphasize that an MCA sets a fixed total cost from day one.

Interest rates, expressed as an Annual Percentage Rate (APR), reward you for early repayment. Paying a traditional loan faster reduces the total interest charged on the balance.

Our data confirms that 2026 SBA loans average between 9.5% and 13% for qualifying businesses.

Factor rates operate completely differently.

Market data for 2026 shows standard US factor rates range from 1.10 to 1.55 for food service businesses.

We see many owners mistakenly interpret a 1.30 rate as a 30% APR.

That multiplier simply dictates the total payback amount. Clearing the balance fast does not save you money.

| Feature | Interest Rate (APR) | Factor Rate (Multiplier) |

|---|---|---|

| Cost Basis | Accrues on outstanding principal | Fixed total cost set at signing |

| Early Payoff | Saves money on interest | Usually offers no financial benefit |

| 2026 US Average | 9.5% to 13% (SBA Loans) | 1.10 to 1.55 (MCA Providers) |

Our partners rarely see standard contracts offering early-payoff discounts.

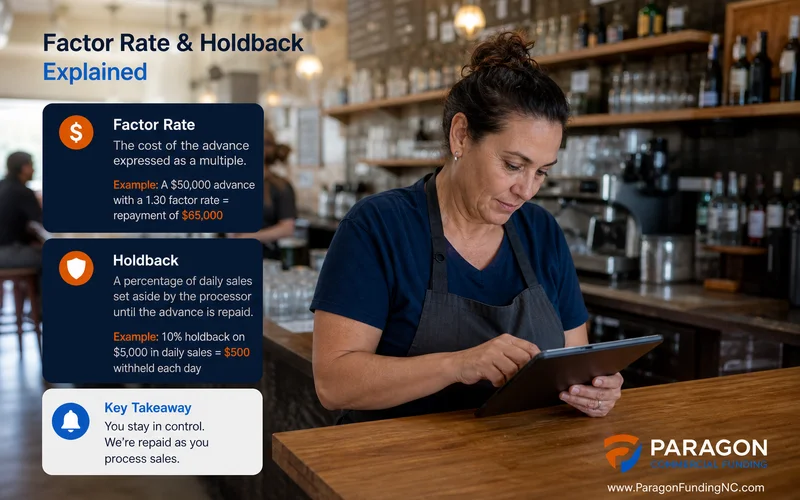

Let’s look at a concrete $50,000 scenario with a 1.30 factor rate. Your total required repayment is $65,000, creating a fixed cost of capital at $15,000.

Our clients must pay that same $65,000 whether the term lasts six months or twelve months.

Converting Factor Rate to Equivalent APR

Converting a factor rate into an effective APR requires calculating the fixed fee against your actual repayment timeline. A shorter repayment window dramatically spikes your equivalent annual interest.

We use a simple formula to help clients compare these costs directly against working capital options.

Consider a real-world emergency, like replacing a $35,000 walk-in freezer on a Friday. You secure a 1.30 factor rate and repay the $10,500 cost over seven months.

Our calculations show that timeline pushes your effective APR to approximately 75%.

Accelerating those sales to repay the amount in just three months pushes the effective APR well over 150%. This shifting math proves why an MCA costs significantly more than a standard bank note.

How Daily Repayment Works

Our team knows that daily repayment happens automatically through either a credit card split or a fixed bank withdrawal.

Understanding how mca works restaurant repayment is critical for managing your weekly cash flow. The wrong method can easily drain your operating accounts.

The Card Split Method

Our preferred setup for seasonal shops is the card split, also called a holdback.

This structure routes a fixed percentage of your daily merchant processing sales directly to the funder. Integration with systems like Square or Toast makes the daily transfer completely automatic.

We always remind owners that a 10% holdback means a $4,000 Saturday results in a $400 repayment.

A slow $1,200 Tuesday drops that payment to just $120. The flexibility prevents missed payments during bad weather days.

The Daily ACH Sweep

Our underwriters typically see ACH sweeps used when a restaurant lacks consistent credit card volume.

A daily ACH sweep deducts a rigid dollar amount from your business checking account every single weekday. This acts much like a daily loan payment, ignoring your actual daily revenue.

We warn clients that a slow rainy weekend will not stop the agreed-upon $250 ACH pull on Monday morning.

The fixed debit amount creates significant risk if sales suddenly drop. Careful forecasting is mandatory for this specific repayment type.

Holdback Percentage Range

We track current market data showing 2026 holdback percentages for American restaurants range between 10% and 20% of daily card receipts.

Your specific percentage gets locked in at signing to ensure you clear the balance within the provider’s target timeline. Providers dictate this withholding amount based on a few core metrics.

- Total Advance Size: Larger dollar amounts require higher daily withholding to hit the standard 6 to 12-month target.

- Daily Card Volume: High-volume operators can satisfy timelines using a much smaller daily slice.

- Business Risk Profile: Strong credit files and consistent deposits help negotiate lighter daily burdens.

Our advisors emphasize getting the factor rate holdback explained clearly before signing anything.

Many owners incorrectly assume the 15% daily holdback is the actual fee structure. That percentage just controls the speed of repayment, not the total cost of the capital.

We recommend calculating exactly how losing up to one-fifth of your daily card revenue will impact payroll.

What to Watch For Before You Sign

Failing to read the fine print in an MCA contract can lead to frozen bank accounts and severe legal trouble. The speed of approval often causes owners to skip past critical default clauses.

We review these documents daily and look for several specific red flags.

Critical contract elements require your full attention before funding. Legal consequences escalate rapidly if you violate the terms.

Our legal partners highlight these primary contract risks.

- Stacking Restrictions: Most funders expressly prohibit taking a second advance from competitors like Funderial or Reliant, and doing so triggers an immediate default.

- UCC Liens: A Uniform Commercial Code lien allows the funder to claim your business assets without prior warning if payments fail.

- Confessions of Judgment (COJ): Some state contracts include a COJ, allowing the lender to obtain a legal judgment against you instantly upon default.

- Personal Guarantees: These agreements usually require you to back the funding with your own personal assets.

Always calculate the total dollars paid rather than focusing strictly on the manageable daily amount.

State regulations frequently change how these clauses are enforced.

We must note that the SBA officially stopped refinancing MCA debt in 2025.

This structural change removes a common exit strategy for overleveraged food service operators. Carefully evaluating the risk is your best defense.

When MCA Is the Right Tool

Our team routes clients toward these specific products only when speed or credit issues rule out bank financing.

An MCA is the right tool when you need capital in under 48 hours to solve an immediate, revenue-threatening emergency. Traditional working capital products simply cannot move fast enough to fix a broken hood system on a Friday.

We find this structure makes sense in a few distinct scenarios.

- Sub-600 FICO Scores: Poor personal credit often disqualifies you from standard loans but rarely kills an MCA approval.

- Seasonal Revenue Dips: The daily-flex repayment of a card split perfectly matches inconsistent, highly seasonal sales patterns.

- Extreme Speed Requirements: You can secure $50,000 in 24 hours, whereas a standard SBA Express loan takes four to six weeks.

- Cash-Heavy Operations: Traditional bank statement underwriting often struggles with these models, making alternative revenue-based funding necessary.

Businesses with excellent credit and time to spare should look elsewhere. Traditional working capital loans cost dramatically less for qualified applicants.

Our platform evaluates your exact 2026 data profile to direct you to the most affordable product.

Next Step

If you determine this structure fits your immediate operational needs, you can pre-qualify in 60 seconds.

The system performs a soft credit pull that will not impact your FICO score.

Our North Carolina funding team is standing by at (910) 685-8872 to walk through a direct cost comparison.