The Honest Cost Picture

As independent restaurant operators know, there is a big difference between the advertised rate of a funding offer and what actually leaves your bank account each month. We see this confusion regularly when founders analyze an mca vs working capital loan cost breakdown. The structural difference between merchant cash advances and working capital loans is real and meaningful.

With 2026 Toast profitability data showing average restaurant margins hovering between 3% and 5%, every dollar spent on financing directly cuts into your tight bottom line. Our goal is to help you protect that margin by looking at the true cost of merchant cash advance products.

You must ask which product fits your actual qualifying profile, and if lower credit or seasonal sales make a standard loan tough, our MCA approval with lower credit or seasonal revenue guide explains the revenue-based path. Let’s look at the data and explore practical ways to respond when you need capital fast.

A Direct Cost Comparison: MCA vs Working Capital Loan Cost

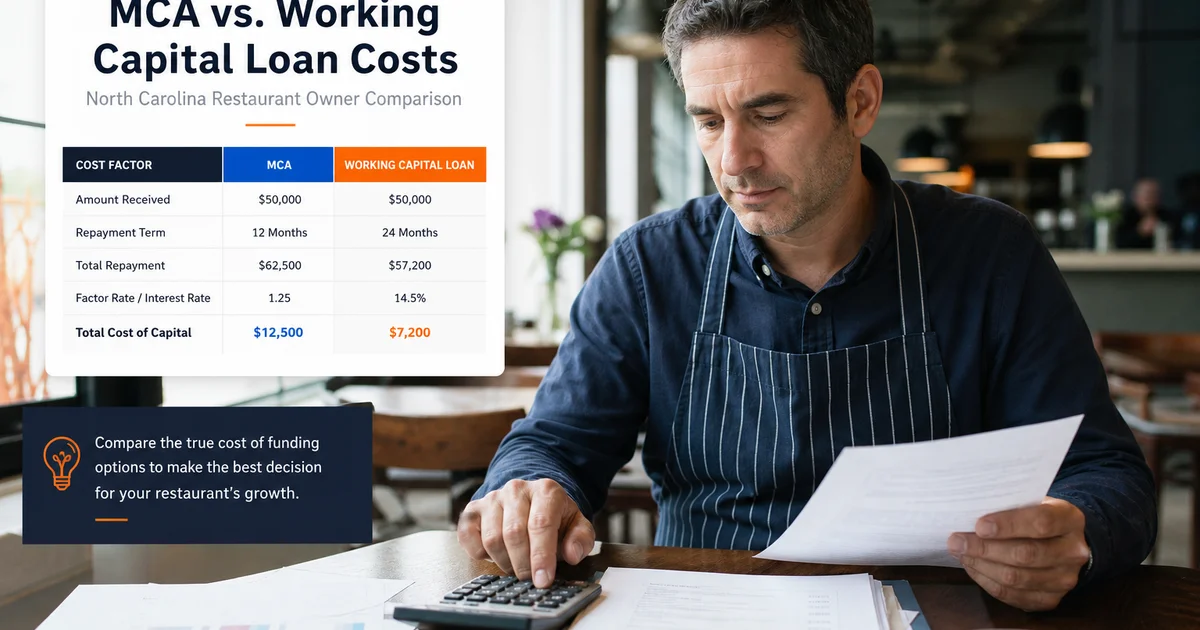

To make this practical, let’s take a standard $50,000 funding amount. We regularly review offers for operators, and the industry average MCA factor rate currently sits at 1.25. The numbers below show the stark reality of how that translates to your cash flow.

This side-by-side breakdown highlights the true cost difference. Our team uses these specific calculations to help clients make informed decisions.

| Feature | Working Capital Loan | Merchant Cash Advance (MCA) |

|---|---|---|

| Terms | 12-month term, 25% APR | $50K advance, 1.30 factor rate |

| Payment Structure | ~$4,750 fixed monthly payment | Daily ACH or split repayment |

| Estimated Timeline | 12 months exactly | ~10 to 14 months (sales dependent) |

| Total Interest/Fee | ~$7,000 total interest | $15,000 fixed fee |

| Total Repayment | ~$57,000 | $65,000 |

That gap represents roughly $8,000 more out of pocket with the MCA. You are paying a massive premium for the alternative structure. We strongly advise operators to calculate this exact dollar difference before signing anything.

Why the MCA Costs More

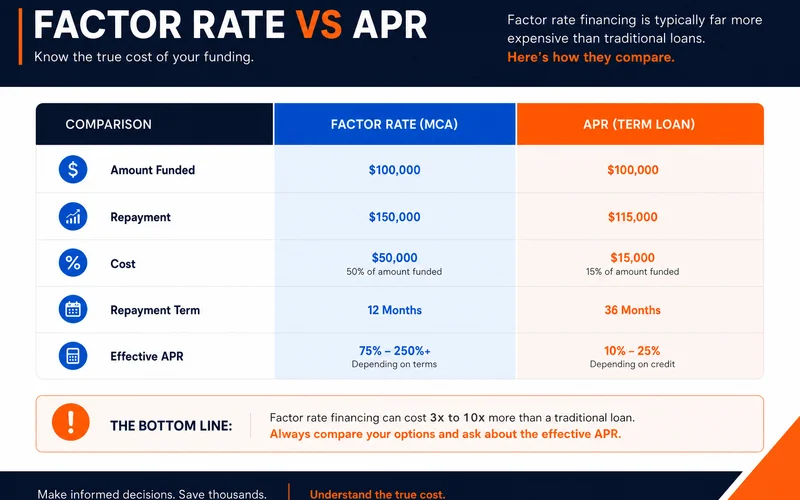

The higher cost of an MCA reflects real structural differences in how the money is deployed. We need to look closely at the risk models lenders use. Comparing the mca factor rate vs apr data explains the gap, as 2026 figures from Luca AI show MCAs generating effective APRs ranging from 40% to over 350%.

This extreme pricing accounts for the specific risks the funding company assumes. Our experience shows that four key factors drive this premium.

Lower Credit Thresholds

Alternative lenders accept higher-risk borrowers with lower credit scores and shorter operating histories. The elevated factor rate prices in the higher default rate they expect. We see many approvals for operators with FICO scores below 600.

No Collateral Structural Enforcement

These products are legally structured as a purchase of future receivables, not secured loans. This structure provides fewer enforcement levers than a standard unsecured working capital loan. Our legal reviews confirm that this lack of collateral drives up the lender’s risk profile.

Daily-Debit Operational Risk

Daily ACH or credit card split repayment is operationally complex to manage. The higher cost partially funds the heavy infrastructure required to process hundreds of micro-transactions a month. We know that managing daily cash flow fluctuations adds significant stress to your operations.

Speed and Accessibility

Faster funding carries a steep premium. We often see same-day funding for MCAs, while working capital loans follow a standard one to three day timeline. The cost difference is reasonable in light of what the product actually does.

Pretending these two products are equivalent does a massive disservice to independent operators.

When MCA Is Worth the Premium

There are a few specific scenarios where paying the higher cost is genuinely justified. We direct clients to MCAs when traditional avenues are closed or when speed is a survival mechanism. An expensive approval is sometimes better than a cheap rejection.

Our team has identified four situations where the math actually makes sense for an independent restaurant.

You Miss Working Capital Thresholds

Traditional lenders maintain strict minimums. You might have personal credit below 600, a time-in-business under one year, or revenue patterns that fall short of $150K annualized. We view the higher cost of an MCA as the necessary price of access when this is your only unsecured funding option.

Equipment Failures Demand Immediate Cash

When a timeline genuinely matters more than cost, speed is everything. We recently saw industry reports from Penguin Trailer noting that a walk-in cooler failure can cause $3,000 to $15,000 in spoiled inventory within hours. If you need a $5,000 compressor replaced today to save $15,000 in food, paying a steep premium for same-day capital is a smart, profitable decision.

Severe Revenue Seasonality

Coastal North Carolina operators understand extreme revenue swings. We see operators with dramatic peak-to-trough patterns between the busy April to August summer season and the dead of winter. An MCA naturally flexes with this curve because daily card-split payments drop automatically when your sales slow down.

Strategic Funding Stacking

Sophisticated operators sometimes use a smaller MCA alongside a larger working capital or equipment financing package. We see this tactic used to capture specific, time-sensitive vendor discounts. The high cost remains contained because the fast-cash portion of the total debt is relatively small.

When MCA Is Not Worth It

For operators who qualify for traditional working capital, the alternative product is rarely justified. We look closely at current market data, and average bank term loans sit around 5.5% to 11% in 2026. Taking a 40% effective APR when you qualify for a 10% rate is a severe unforced error.

Our internal routing guidelines send eligible operators away from high-cost advances. Take the traditional route if you meet these exact criteria:

- You meet the 600 credit score minimum.

- Your restaurant has been operating for over one year.

- You demonstrate predictable monthly revenue exceeding $150K annualized.

- You can afford to wait one to three days for the funds to clear.

- You want the cleanest, most predictable cost structure.

Take the working capital loan if your profile matches that list. We route eligible operators to these simpler products as a matter of course. You will pay less and enjoy predictable, fixed monthly payments.

The Comparison Calculator Exercise

Evaluating two vastly different financing structures requires a standardized approach. We advise every client to stop looking at the monthly payment in isolation. New 2026 disclosure laws in states like New York and California now force lenders to reveal the true APR, but you still need to run the raw numbers yourself.

Our diagnosis call walks through this exact comparison honestly. If you are comparing offers at your desk, follow this five-step calculation to find the truth.

- Calculate total dollars repaid: Look at the absolute final number under each structure, not just the monthly or daily draw.

- Isolate the total cost: Identify the exact dollar amount of the interest charge or the factor cost premium.

- Map the repayment timeline: Compare the fixed 12-month loan against the estimated 10 to 14-month MCA window.

- Assess the operational fit: Decide if your cash flow can handle a daily card split or if you need a fixed monthly payment.

- Determine approval probability: Be realistic about whether you actually qualify for both options before wasting time on an application.

Run those exact numbers. We find that the right answer usually becomes obvious once the total cost is isolated on paper.

A Worked Example

Let’s look at how this plays out for two different businesses in North Carolina. We use these real-world profiles to demonstrate how qualification dictates your final choice.

Scenario A: The Charlotte Startup

A Charlotte restaurant operator has 18 months in business, $200K in annual revenue, and a 580 credit score. We know that standard working capital is unavailable because their credit is below the strict 600 minimum. The alternative cash advance is their only path forward.

The cost premium of taking the advance over a hypothetical equivalent loan is real. However, that cheaper loan does not actually exist for them. We view this as a choice between high-cost capital or zero funding, which means the advance wins by definition.

Scenario B: The Established Wilmington Operator

Now consider a Wilmington operator with five years in business, $400K in revenue, and a strong 720 credit score. Both financial products are readily available to this established business. We see a massive cost gap here, often exceeding $8,000 on a standard $50K deal.

This specific scenario requires a traditional approach. Our team routes this Wilmington operator directly to a working capital loan. That is the exact diagnosis logic you must apply to your own restaurant.

Next Step

Evaluating your mca vs working capital loan cost options should never be a guessing game.

Pre-qualify in 60 seconds and we will route your application to the right product based on your actual qualification profile. Our process ignores the structure with the highest broker margin and focuses entirely on what benefits your restaurant.

Call (910) 685-8872 today to get started.