The Short Answer

We see the same financing dilemma happening repeatedly across the North Carolina hospitality scene. Owners constantly debate whether to take a standard loan or a fast cash advance.

You know exactly how stressful it gets when a walk-in cooler fails right before a massive holiday weekend. The average U.S. restaurant profit margin sits at a tight 3% to 5% in 2026.

Our team understands that a margin this thin makes every single funding choice critical to your survival. That reality is why a standard working capital loan usually beats a merchant cash advance if your credit score allows it. Fixed-term loans offer predictable payments that protect your baseline cash flow.

“Choosing the wrong capital structure can erase a month of hard-earned profits overnight.”

We will break down the exact math behind a working capital loan vs merchant cash advance restaurant comparison, helping you pick the best short term restaurant funding option. If you are weighing operating cash against an asset purchase, our working capital vs. equipment financing guide covers which product fits each situation.

The Core Differences

The structural difference between these two funding types dictates how your daily cash flow operates. Choosing incorrectly can create massive stress during slow seasons.

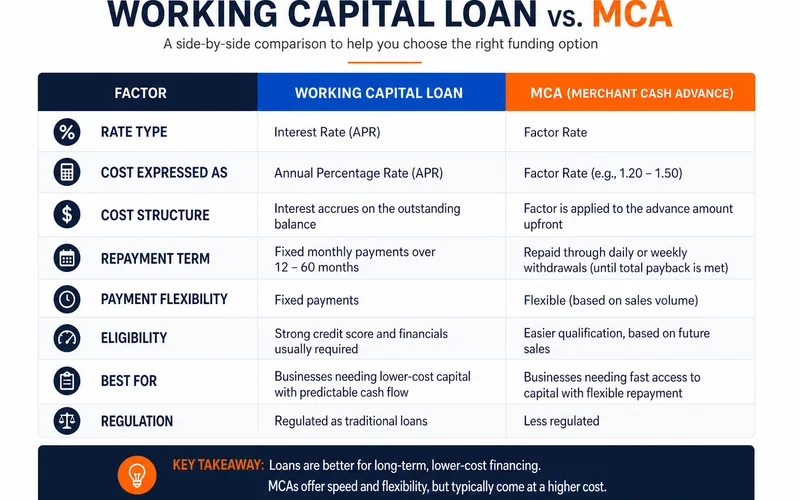

Our clients often confuse these two distinct financial products. A working capital loan operates like a traditional debt instrument with a set end date. An MCA functions as a business transaction where a company buys a portion of your future sales.

We always highlight the approval speed variance between the two choices. Look at the specific requirements and features of each option to see why.

Working Capital Loan Characteristics

- Structure: Fixed dollar amount with a set term up to 18 months.

- Cost: APR-based pricing, with prime options running around 9.75% to 13.25% in 2026.

- Payment: Predictable monthly amortization.

- Requirements: Minimum one year in business, $150,000 in revenue, and a 600 FICO score.

- Timeline: Closes in one to three days for clean files.

Merchant Cash Advance (MCA) Characteristics

- Structure: Fixed dollar amount with no defined term.

- Cost: Uses a factor rate typically ranging from 1.10 to 1.55 instead of an interest rate.

- Payment: Daily card split or ACH sweep that flexes with your daily revenue.

- Requirements: Strong card-processing history and a much lower credit threshold.

- Timeline: Often provides same-day or next-day funding.

Our experience shows that the payment structure matters immensely for volatile businesses. A loan requires the same flat payment on a dead Tuesday as it does on a packed Friday. An MCA payment scales directly with your daily sales volume.

Cost Comparison

Comparing APR to a factor rate requires some straightforward math. You cannot look at these two numbers at face value.

Our finance experts see owners miscalculate these figures daily. A factor rate is a fixed multiplier applied to your principal at signing, meaning you cannot save money by paying it off early. An APR calculates interest over time, rewarding you for faster repayment.

We built a direct comparison to show the exact dollar difference on a standard $50,000 advance. The MCA effective APR can quickly skyrocket anywhere from 40% to over 300% depending on how fast you repay the balance.

Cost Breakdown on $50,000

| Feature | Working Capital Loan | Merchant Cash Advance |

|---|---|---|

| Stated Rate | 25% APR | 1.30 Factor Rate |

| Term | 12 Months | Estimated 12 Months |

| Total Cost of Capital | $7,000 (Interest) | $15,000 (Fixed Fee) |

| Total Repayment | $57,000 | $65,000 |

Our routing process usually pushes qualified applicants to the loan option because of this massive $8,000 difference. The MCA clearly carries a higher price tag. The tradeoff gives you lightning-fast speed and a flexible repayment schedule based entirely on your revenue.

When the Loan Wins

For operators who qualify, the loan wins on cost almost every single time. It remains the absolute gold standard for stable operations.

Our team recommends this path for restaurants prioritizing long-term financial health. The standard working capital loan size ranges from $35,000 to $120,000 across the U.S. market. Recent industry data shows that 42% of operators entered 2026 completely unprofitable, making cheap capital essential.

We know that keeping your debt costs low is a mandatory strategy for survival. You should pursue a standard term loan under these specific conditions:

- You meet the 600 FICO credit score baseline.

- Your restaurant has a solid one-year operating history with $150,000 in annualized revenue.

- Your monthly sales volume is highly predictable with low seasonality.

- You can easily absorb a fixed monthly payment into your current budget.

- You have a three-day window to wait for funding and closing.

Our primary goal is to match most established North Carolina operations with this product. It provides the cleanest cost structure and the most predictable repayment model available.

When the MCA Wins

The merchant cash advance serves as a highly effective tool for very specific scenarios. You should view it as a specialized financial instrument rather than a daily operating account.

Our underwriting team frequently utilizes this product when traditional banks say no. North Carolina tourism hit a record $36.7 billion in 2024, creating massive summer revenue spikes for coastal towns. This extreme seasonality makes fixed loan payments dangerous during the slower winter months.

We route specific files to an MCA based on a few distinct operational advantages. These unique benefits include:

- Credit Scores Below 600: Working capital requires a 600 minimum score. An MCA ignores your personal FICO and looks strictly at your business revenue history.

- Extreme Seasonality: Your repayment uses a daily holdback rate, typically between 10% and 25% of your card sales. A slow Tuesday requires a tiny payment, while a slammed Saturday clears a larger portion of the balance.

- Same-Day Emergency Funding: A standard loan takes up to three days to close. An MCA can drop funds into your account the exact same day you apply.

- Heavy Cash Operations: You might have strong sales that do not deposit cleanly into a business checking account. An MCA provider will underwrite your file based heavily on your card-processing terminal data.

An MCA is a strategic choice, not a last resort. You justify the higher cost of this product through its structural flexibility and immediate access to emergency capital. We help you weigh these benefits against the actual price tag before you sign anything.

A Worked Example

Seeing the exact numbers side-by-side clarifies how mca vs working capital comparisons play out in reality. Hard data removes the emotion from the borrowing process.

Our loan officers recently reviewed two different coastal North Carolina operators who both needed $40,000 for pre-season inventory. They run very different establishments, meaning they require entirely different financial tools.

Let us look at how their specific profiles dictated their funding paths. The math clearly shows why each owner took a separate route.

Operator A: The Established Veteran

- Profile: Five years in business, $400,000 annual revenue, and a 720 credit score.

- Result: Qualifies for working capital easily.

- Terms: A 12-month loan at 22% APR generates about $4,800 in total interest.

- Repayment: The total payback equals $44,800, with a predictable monthly payment of $3,733.

Our team immediately recommended the loan for Operator A because it offers the absolute lowest cost. The operator had strong credit and highly predictable cash flow to easily handle the fixed monthly expense.

Operator B: The New Arrival

- Profile: 14 months in business, $180,000 annual revenue with strong card sales, and a 580 credit score.

- Result: Cannot secure a standard loan due to the FICO score cutoff.

- Terms: Qualifies for an MCA at a 1.28 factor rate on the $40,000 advance.

- Repayment: The total fee is $11,200, bringing the total payback to $51,200. This amount is collected daily via card splits over an estimated 12 months.

We secured the MCA for Operator B because it was the only viable path to buy their seasonal inventory. The higher cost was entirely justified by the approval access and the revenue-based daily payment structure. Both operators walked away with the exact right product for their immediate business needs.

How to Tell Which Fits You

Running a quick self-assessment will reveal your best short term restaurant funding option. You do not need to guess which product fits your profile.

Our application data shows that meeting specific benchmarks secures the cheapest capital. A FICO score of 600 remains the hard dividing line in 2026 for accessing tier-one commercial lending rates. Lenders also require a clean banking history with strong, consistent daily balances.

We suggest using this simple checklist to determine your immediate eligibility for prime funding. Review these metrics before submitting any paperwork:

- Time in Business: You must have at least one full year of operational history.

- Revenue Baseline: Your annualized gross revenue must exceed $150,000.

- Credit Health: Your personal FICO score must be 600 or higher.

- Banking History: Your business checking account cannot show excessive negative days.

The automated system will route you directly to a working capital loan if you check all four boxes. You can pre-qualify in 60 seconds, and you will likely close the loan in a matter of days.

Missing one or two of these requirements shifts your profile to a merchant cash advance. The MCA utilizes the exact same 60-second pre-qualification process and relies on a soft credit pull that will not harm your score. We will review your file and point you to the exact product that matches your unique metrics.

Next Step

You now understand the complete breakdown of a working capital loan vs merchant cash advance restaurant funding decision.

Pre-qualify in 60 seconds and our team will route you to the exact product that fits your specific financial profile. Taking this step requires no commitment and protects your credit.

You can also call (910) 685-8872 to discuss your options directly with a local funding specialist.