We know exactly how hard it is to secure funding for an independent restaurant right now. The National Restaurant Association projects US industry sales to hit $1.55 trillion in 2026. Grabbing your share of that market requires cash for payroll, inventory, and sudden equipment failures. Our team at Restaurant Financing Pros NC sees operators miss out on growth simply because traditional banks demand massive collateral and weeks of paperwork. This guide breaks down our exact restaurant working capital requirements. Let’s look at the three criteria you need to meet. The following breakdown explains how to calculate your eligibility and exactly what to do if you fall short.

The Three-Number Test

Qualifying for a fast cash injection requires hitting three specific benchmarks: one year in business, $150,000 in revenue, and a 600 credit score. The U.S. Bureau of Labor Statistics recently reported that 83% of restaurants survive their first year in 2026. This data proves that early-stage operators are highly resilient. We built our underwriting model around this reality to keep things accessible. Here are the three quick checks:

- One year in business (minimum)

- $150,000 minimum yearly revenue (demonstrable in bank statements)

- 600 minimum credit score (verified via soft pull during pre-qualification)

You are a great fit for funding if you hit all three of these targets, and because none of this requires pledging assets, our unsecured restaurant working capital guide explains how no-collateral funding actually works. The pre-qualification process takes 60 seconds and returns a clean read on approval and structure. We require zero hard credit pulls to see your offer.

What Each Requirement Means

Every requirement protects both your cash flow and the lender by verifying your business stability. Understanding the reasoning behind these numbers helps you build a stronger application. We look for stability and recent momentum above all else.

One Year in Business

Your business must be operating for at least 12 months to qualify. The clock starts at your very first revenue deposit, not the date of your business formation. A restaurant that opened its doors in May 2025 officially hits the 1-year mark in May 2026.

Our underwriters use this timeline because that first year separates proven concepts from unproven ideas. Most restaurants that survive this initial 12-month period establish a predictable cash flow pattern.

$150K Yearly Revenue

This threshold represents annualized revenue based on your recent operating history. A $150,000 annual requirement breaks down to just $12,500 in monthly sales. Fast-casual concepts in 2026 regularly generate between $750,000 and $1.5 million annually.

We look at the trailing 3 to 12 months of bank statements to verify these deposits. Cash-heavy businesses sometimes struggle to document this threshold if deposits do not match actual sales. Working with your accountant to digitize cash sales solves this documentation issue quickly.

Our funding specialists will help you review your deposits to find the best qualification path.

600 Minimum Credit Score

This refers to the personal FICO score of the primary business owner. The Small Business Administration traditionally requires a minimum credit score of 650 for their 7(a) loans in 2026. We set our minimum at 600 to provide options for operators who fall outside that strict banking standard.

Below a 600 score, standard term financing is rarely the right structure. A merchant cash advance often serves as the perfect alternative in these situations. We will review your profile and route you directly to the product that fits your score.

What If You Don’t Hit One of These?

Missing a single requirement means we will need to pivot you to an alternative structure like equipment financing or a merchant cash advance. The average independent restaurant requires up to $500,000 in startup capital before serving a single dish. We understand that newer operators might need cash before hitting the one-year mark. Here is a breakdown of common scenarios and alternative paths.

| Feature | Standard Working Capital | Merchant Cash Advance (MCA) |

|---|---|---|

| Minimum Time in Business | 12 Months | 3 to 6 Months |

| Minimum Credit Score | 600 FICO | 500+ FICO |

| Revenue Requirement | $150,000/year | Flexible (Revenue-based) |

| Repayment Structure | Fixed periodic payments | Percentage of daily sales |

Alternative Solutions by Scenario

Startups under one year in business cannot access traditional term loans. Startup-friendly equipment financing or a merchant cash advance offers a viable alternative. We match early-stage operators with lenders who specialize in newer concepts.

A file with strong credit can sometimes pass underwriting if revenue sits closely around $130,000. An MCA is typically the smarter choice for revenue below that mark. Our partners fund revenue-based MCA products on the exact same day of approval.

Applications missing two out of three requirements face a very steep climb for standard financing. We will suggest alternative structures honestly rather than wasting your time with false hope.

No Collateral, No Out-of-Pocket Fees

Traditional bank loans frequently require business owners to pledge their homes or put down 20% in cash. Our financing structure removes these massive hurdles completely by issuing unsecured loans with zero upfront costs. These unsecured loans rely entirely on the strength of your recent cash flow and credit profile. Two specific features make this product highly attractive to restaurant owners.

No Personal Collateral Required

Lenders do not take a lien on your expensive kitchen equipment or personal real estate. The loan remains completely unsecured from start to finish. We base the entire underwriting decision on your revenue consistency and credit history. This protects your personal assets if the business faces unexpected market shifts.

Transparent Cost Structure

You will never pay an application fee or an upfront origination cost. The total cost of the financing is built directly into the repayment term. Our advisors disclose every single dollar before you sign the final agreement.

Average business loan interest rates in 2026 span a massive range from 6% to over 20%. Operators sometimes doubt this fee-free structure until they see the contract in writing. We guarantee this level of transparency because it represents the modern standard for alternative lending.

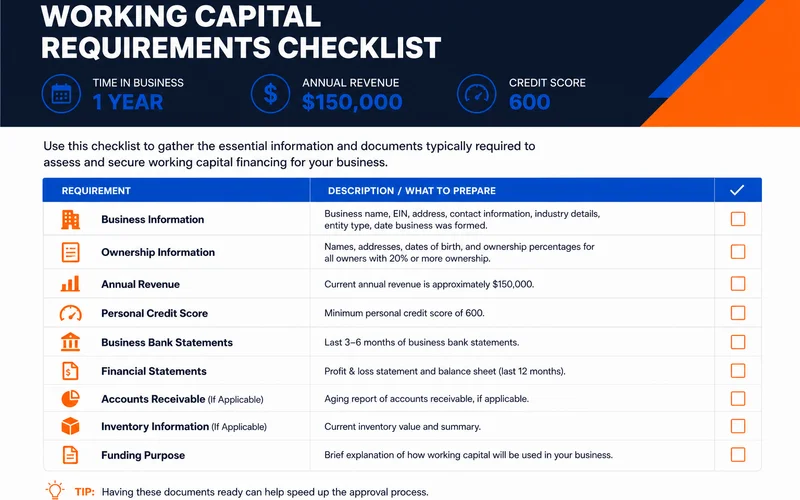

Documentation Required

A complete file only requires three months of bank statements, basic business info, and a soft credit pull. Gathering financial documents for an SBA loan often takes weeks of back-and-forth emails. We eliminate that massive paperwork burden completely. A complete file requires only a few basic items to reach the underwriting desk:

- 3 months of business bank statements (PDF exports from your online banking are fine)

- Basic business information (entity name, ownership, business address, tax ID)

- Voided check or banking information for funding deposit

- Soft credit pull authorization (handled during pre-qualification)

You never need to submit tax returns or P&L spreadsheets for standard working capital files. The simplicity of this checklist is exactly why working capital funds in just one to three days. We cut out the red tape so you can get back to running your kitchen.

What “Yearly Revenue” Actually Means

The $150K revenue requirement represents an annualized projection based on your most recent three to twelve months of sales. Seasonal shifts in the restaurant industry can dramatically alter month-to-month cash flow. We use a trailing formula to ensure recent strong performance is recognized.

You clear the threshold if you have operated for 12 months and collected $200,000 total. A restaurant operating for 9 months with $135,000 in sales hits an annualized rate of $180,000. Our team accepts this annualized pace even if the calendar year has not officially closed.

Most underwriters analyze the trailing three months to prevent older, slow periods from masking your current success.

A busy summer patio season can easily push your annualized rate into the approval zone.

We calculate a trailing three-month total of $40,000 as $160,000 annualized. This mathematical approach provides a much fairer picture of your current momentum.

A Self-Qualification Quick Check

Answering yes to five simple questions confirms your eligibility for funding today. Many owners ask us, “do I qualify working capital based on my current sales?” We highly recommend completing this rapid checklist before moving to the next step. Run through these five statements right now:

- In business at least 12 months

- Revenue (annualized) at least $150K

- Personal credit at least 600

- Business bank account separate from personal

- No active bankruptcy filing

Checking all five boxes means you are a highly qualified candidate for working capital. The next step is to view your specific funding options. Our platform will generate a clear offer without impacting your credit score.

Next Step

Your next step is to complete our 60-second online pre-qualification form. This process uses a simple soft pull that leaves your credit completely unharmed. We are also available by phone at (910) 685-8872 to discuss your specific financial situation. Review your exact working capital qualification restaurant status right now. Start here to secure the cash your restaurant needs to thrive.