All Credit Tiers Means All Credit Tiers

Many restaurant operators feel defeated when traditional lenders reject their applications. Big banks currently approve only about 25% of small business loan requests in 2026. A slight credit dip or a prior bankruptcy often triggers an automatic denial.

Our team at Restaurant Financing Pros NC sees this frustration every day across North Carolina. That rigid banking model leaves hard-working owners without options. You need practical solutions that actually fund your kitchen.

We provide comprehensive restaurant equipment financing across all credit profiles, including:

- Standard restaurant equipment loans for bad credit.

- Alternative lease structures for startups.

- Funding for operators recovering from Chapter 7 or 13.

Credit challenges change the structure of your deal, not necessarily your ability to get funded.

Our goal is to outline those structural trade-offs clearly. Let’s review exactly how credit tiers impact your options and what underwriters need to see.

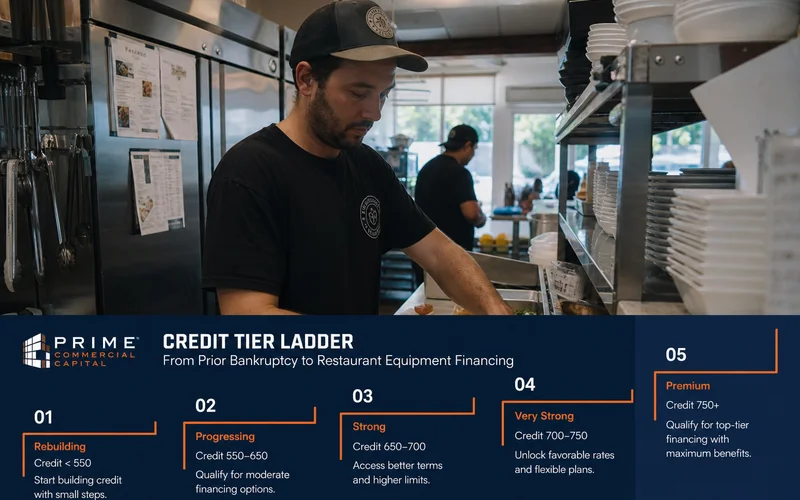

The Tier Ladder, Plain English

The average credit score for a small business owner in the US hovers around 721. Those with lower scores face a different lending reality.

Our underwriting process uses a clear tier system to match your profile with the right structure. Understanding these tiers helps you anticipate the exact terms you will likely receive. Here is how the credit landscape breaks down for restaurant equipment approvals.

| Credit Tier | Score Range | Expected Down Payment | Typical Loan Structures |

|---|---|---|---|

| Prime | 700+ | 0% to 10% | EFA, standard loan, or lease |

| Near-Prime | 640-699 | 10% to 20% | Most structures available |

| Mid-Tier | 580-639 | 20% to 30% | EFA, loans, leases to spread cost |

| Sub-Prime | Below 580 | 30% to 40% | Shorter terms, lease structures |

Chapter 7 or Chapter 13 bankruptcies require a specific approach. Post-bankruptcy files generally need 12 months of clean operational history. We usually require a larger cash injection compared to standard sub-prime profiles to offset the risk.

What Underwriters Actually Look At

A single credit score rarely tells the whole story of your operation. Lenders evaluate several risk factors when reviewing lower-tier files.

Our network analyzes the total health of your business rather than relying on one number.

Operating History and Startup Risk

Time in business heavily influences your approval odds. A five-year-old cafe with a recent credit dip looks very different than a startup facing the exact same issue.

Opening a new independent restaurant often costs between $275,000 and $850,000 in 2026. Underwriters prefer established operations that have already cleared those initial financial hurdles.

Asset Value and Collateral

The type of equipment you buy changes the risk calculation. Hard assets hold strong resale value. A heavy-duty Garland commercial range acts as solid collateral for the lender.

Rapidly depreciating tech assets like a Toast POS system offer almost no secondary market value. Strong collateral can often offset a weak credit profile.

Cash Injection and Vendors

Putting more cash down reduces the lender’s exposure instantly. A substantial down payment frequently opens doors for files that would otherwise face denial.

The seller’s reputation also matters during the underwriting process. Established commercial vendors present far less risk than unknown third-party sellers.

We finance both types of purchases, but the specific vendor affects the terms. Be sure to check our used equipment guide for more details on buying secondhand.

Honest About Rates

Interest rates absolutely increase as credit scores drop. The 2026 SBA Prime rate sits at 6.75 percent.

Standard government-backed loans typically range from 9.5 to 11.5 percent for the strongest borrowers. Our prime-credit operators might secure a 7 to 10 percent APR on a five-year equipment loan.

Mid-tier files generally see rates climbing to the 12 to 16 percent range. Sub-prime profiles and post-bankruptcy approvals cost even more.

These high-risk deals are often structured as leases with effective rates exceeding 18 percent. The total cost of capital varies significantly based on your tier.

The right framing isn’t asking if a rate is the cheapest possible. The right framing is asking if this financing structure allows you to open, expand, and generate new revenue.

You should shift your focus from finding the absolute cheapest money to finding viable capital. Getting denied by every local bank leaves you with zero purchasing power.

A slightly higher rate that allows you to buy a walk-in cooler and open your doors is a smart business decision. We always encourage prime borrowers to shop around, but challenged profiles must prioritize securing the approval.

The Pre-Qual Path

The first step toward funding is a fast pre-qualification. This process uses a soft credit pull that will not impact your FICO score.

We obtain a clear read on your tier, appropriate deal structure, and expected down payment immediately. This happens before you commit to any formal paperwork.

Our pre-qualification review identifies three critical factors upfront:

- Your exact credit tier classification based on recent data.

- The financing structure that best matches your financial history.

- The estimated down payment required to secure an approval.

Lenders in the commercial space specialize in different risk profiles. Our job involves matching your specific file to the correct underwriter right away.

Routing a sub-prime deal to a prime lender only results in a frustrating denial. Proper placement speeds up the entire funding cycle.

What to Have Ready

Speed matters when you need to replace broken equipment or meet a grand opening deadline. Gathering the correct documents upfront prevents unnecessary delays.

Our processing team moves much faster when you submit a complete package on day one. If you want the quickest path through underwriting, prepare these specific items:

- Recent Bank Statements: Supply the most recent three months of your primary business checking account statements.

- Detailed Equipment Quotes: Provide a clear invoice or formal vendor quote for the exact machinery you need.

- Credit Explanations: Write a brief, honest summary of any past bankruptcies, tax liens, or late payment clusters.

- Post-Bankruptcy Proof: Include court discharge papers and proof of current revenue if you are seeking Chapter 7 restaurant financing.

Do not try to hide your credit history from the lender. The underwriting software will flag those events during the background check anyway.

We can match you to a flexible lender much faster if you disclose issues upfront.

Next Step

Finding capital with damaged credit requires working with the right partners. Securing restaurant financing after bankruptcy is entirely possible.

You still have viable options even if your local branch turned you away. Our 60-second pre-qualification relies entirely on a soft credit pull.

This means you can check your true approval odds without any risk to your current score. Give this alternative path a shot today.

We will tell you honestly what kind of terms you can expect. You can Pre-qualify in 60 seconds online or simply call (910) 685-8872.