The Real Trade-Offs

We see many first-time operators wrestle with the exact same financing dilemma before launch.

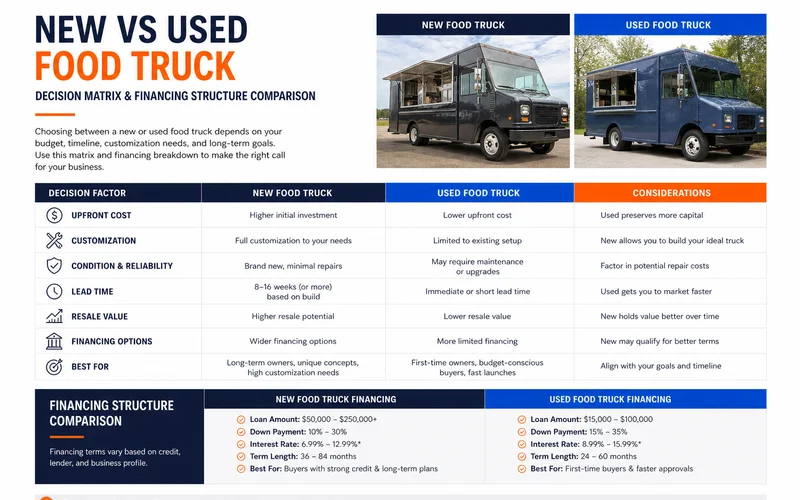

The choice between new vs used food truck financing shapes your entire cash flow model for those critical first two years. Current industry data from 2026 reveals a stark contrast in average purchase pricing:

- Average New Custom Build: $109,500

- Average Used Truck: $46,800

That massive cost gap is real and meaningful.

We help North Carolina restaurant owners get the equipment and working capital they need to open, expand, and stay competitive. Those cheaper upfront prices for used models often mask hidden maintenance costs.

This guide breaks down the true financial trade-offs to help you decide which path fits your concept. You can explore our broader cost to finance a food truck or trailer guide for complete budget ranges, and our food truck and trailer financing hub provides excellent foundational strategies.

New: What the Premium Buys

A new custom food truck on a current-model chassis gets you full warranties, predictable reliability, and the cleanest path to a 60-month or 84-month loan. You are paying a premium of $100K to $250K+ to avoid operational downtime.

Our financing partners prefer new assets because they represent lower collateral risk. This preference translates directly into more favorable loan terms for you.

According to standard commercial depreciation schedules, step vans and food trucks lose roughly 15% to 25% of their value annually. A brand-new truck protects you from inheriting someone else’s deferred maintenance and secures the following benefits:

- Full warranty protection. You receive the chassis warranty from the manufacturer, a fabrication warranty from the builder (typically 1 to 3 years on workmanship), and direct equipment warranty pass-through.

- Predictable reliability. The truck comes with low mileage on the chassis, fresh cooking equipment, and zero service history surprises.

- Exact concept fit. You specify the layout to match your menu instead of retrofitting an awkward existing kitchen.

- Resale value retention. A new build holds a better depreciation curve than a used unit you plan to resell in a few years.

- Strongest financing access. New trucks offer the cleanest underwriting path, and banks frequently extend longer repayment terms.

We recommend planning ahead for the 8 to 16 week custom build queue. Fabrication labor and commercial steel costs have remained high throughout 2026.

The sticker price is firm, but the peace of mind is unmatched.

Used: What You Trade

You might be wondering, should I buy a used food truck? Buying a used mobile kitchen gets you on the road faster for 40% to 60% less upfront capital, but it requires sacrificing warranties and accepting higher maintenance risks.

You must trade peace of mind for immediate market entry. A cheaper sticker price does not eliminate your financial risk.

We advise clients to reserve at least $5,000 to $15,000 in working capital specifically for first-year equipment fixes and unexpected upgrades. A used mobile kitchen from a dealer, a private seller, or an auction delivers these immediate benefits:

- Drastically lower upfront cost for a comparable specification.

- Faster acquisition and launch without sitting in a custom build queue.

- Sometimes pre-permitted if it operated in your county recently.

- Established concepts that come with community brand history.

In exchange for these benefits, you must accept certain compromises:

- Limited or zero warranty on the chassis, structural fabrication, and cooking equipment.

- Higher service reserve required for the first 24 months of operation.

- Mandatory inspection costs before you finalize the purchase.

- Concept compromise because the truck was built for someone else’s specific workflow.

- Variable mechanical reliability depending on prior service records and oil change frequency.

Financing Differences

New food trucks qualify for the longest terms and lowest rates through Equipment Finance Agreements, while older used trucks often require larger down payments and shorter repayment periods. The age of the asset directly dictates your loan structure.

We process applications for both new and used food trucks through our trusted network. The specific underwriting guidelines vary significantly based on the condition of the vehicle.

With an Equipment Finance Agreement, you own the equipment from day one, which allows you to claim substantial tax deductions under Section 179 rules. This structure is incredibly popular for both new and recent-model used trucks.

| Equipment Type | Typical Down Payment | Standard Term Length | Underwriting Focus |

|---|---|---|---|

| New Custom Build | 0% to 10% | 60 to 84 months | Cleanest path, highest approval rates. |

| Used (Dealer) | 10% to 20% | 48 to 60 months | Treated like new if age/hours are low. |

| Used (Private/Auction) | 15% to 25% | 36 to 60 months | Requires clean title and inspection report. |

| Used (7-10+ Years Old) | 25% to 40% | 36 to 48 months | Terms strictly match remaining useful life. |

Our team sees the highest success rates when operators match their loan term to the expected lifespan of the truck.

You do not want to be paying off a five-year loan on a vehicle that needs a full engine replacement in year three.

The Inspection Step

A pre-purchase inspection is the single most important step when buying a used food truck to prevent catastrophic mechanical or health code failures. You must hire a qualified commercial inspector before finalizing any transaction.

We tell every client that skipping the inspection is the fastest way to bankrupt a new mobile food business. NSF International certification is strictly required for commercial food service equipment across the United States.

Local health departments will fail your inspection immediately if you lack NSF-approved sinks, proper refrigeration, or correct surface materials. A solid pre-purchase inspection costs $400 to $1,500 depending on the scope of the review.

Make sure your inspector evaluates these critical areas:

- Chassis and engine condition. Check for rust, verify mileage, and review accident history.

- Fabrication structural integrity. Look for roof leaks, floor rust, and wall compromises.

- Equipment functionality. Fire up every single piece of cooking equipment and test the refrigeration recovery times.

- Generator hours and health. Check how long the generator has run and when the oil was last changed.

- Electrical and plumbing systems. Confirm water line integrity, test for gas leaks, and verify a dedicated handwashing sink is present.

Our inspectors consistently flag improper fire suppression systems, like a missing Class K extinguisher, as a top reason for failed health department walk-throughs.

Spending a thousand dollars upfront can easily save you tens of thousands in surprise repairs.

Decision Framework

Your choice between new and used depends entirely on your available capital, timeline, and mechanical comfort level. This simple framework matches different operational profiles with the right equipment strategy.

We created this breakdown to help you map your business model to the appropriate financing risk.

Consider these common scenarios before applying for a used food truck loan.

- Tight budget, willing to do maintenance work, established operator. Used often wins because you have the skills to manage the upkeep.

- First-time operator, need reliability, want concept-specific build. New often wins because it eliminates operational guesswork.

- Need to start fast for festival season or a contract. Used available immediately beats waiting on a custom build.

- Multi-unit operator scaling a fleet. Often a mix works best, using new for the flagship and used for additional regional units.

- Specialty concept like BBQ, coffee, or very specific cuisine. New custom is often the only way to get the exact plumbing and ventilation build.

A Worked Example

Financing a $65K used trailer over 48 months requires lower overall debt, while a $130K new build over 60 months secures reliability at a higher monthly cost. Let us compare the exact numbers for a growing barbecue operation.

We can look at an established operator scaling from one truck to two. They have two primary paths to secure their second unit.

| Scenario | Purchase Price | Down Payment (20%) | Loan Term | Primary Advantage |

|---|---|---|---|---|

| Buy Used Trailer | $65,000 | $13,000 | 48 Months | Lower monthly payment, faster ROI. |

| Buy New Custom Truck | $130,000 | $26,000 | 60 Months | Maximum reliability, full warranty. |

With the used option, the payments remain highly manageable from the first truck’s revenue while the second unit ramps up. The business assumes the maintenance risk but keeps fixed costs low.

Our alternative scenario with the new truck carries noticeably higher monthly payments. The long-term reliability and asset resale value provide a strong safety net.

Neither approach is universally right or wrong. You must match the financial structure to your specific operator profile and cash reserves.

Next Step

Choosing the right path requires knowing exactly what you qualify for before making an offer. Whether new or used, pre-qualifying first gives you visibility into approval and structure.

We utilize a soft credit pull that has absolutely no impact on your personal credit score. This gives you risk-free insights into your purchasing power.

Take the guesswork out of your expansion today. Call (910) 685-8872 to walk through your specific deal with a financing expert.